SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

The overall economy grew at just a 1.1 percent annual rate in the first quarter, as inventories were a major drag on growth. Weak inventory accumulation in the quarter (inventories actually fell slightly) subtracted 2.26 percentage points from growth in the quarter. Final demand, which excludes changes in inventories, increased at a 3.4 percent annual rate.

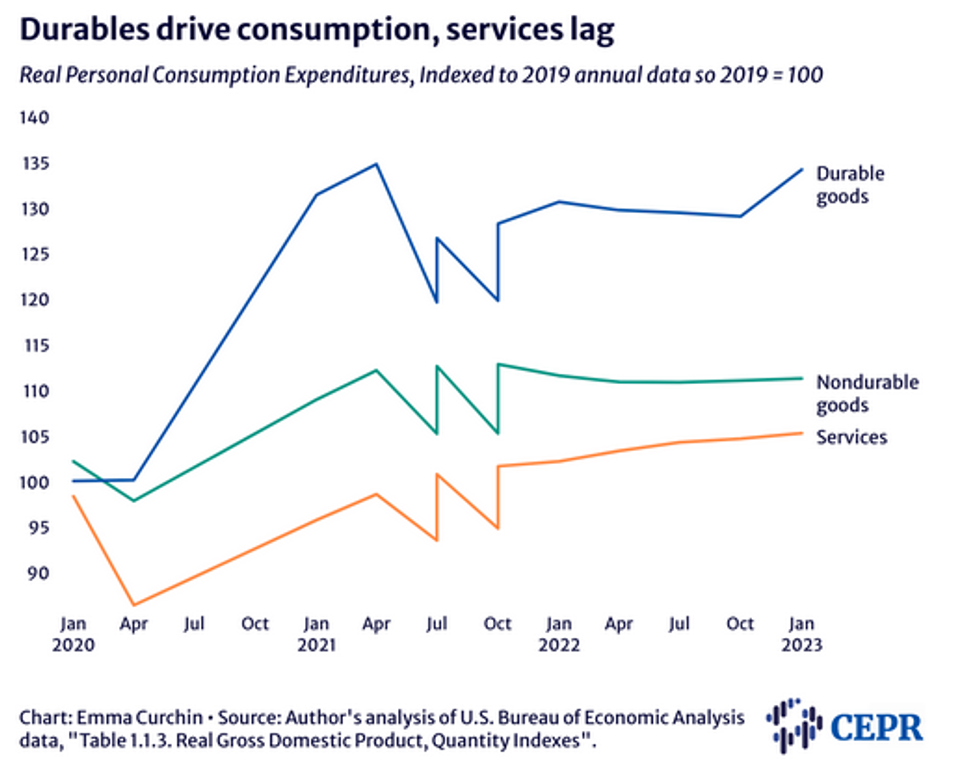

Consumption Grows at a 3.7 Percent Rate, Driven by Strong Car Sales

After slowing to just a 1.1 percent growth rate in the fourth quarter, consumption growth rebounded in the first quarter. The major factor was a 16.9 percent growth rate in durable goods consumption after three quarters of modest declines. This jump was in turn driven by vehicle sales, which rose at a 45.3 percent rate in the quarter.

This sort of jump will not be repeated in future quarters, and in fact, car sales may be somewhat of a drag in the rest of the year. Non-durable goods grew at just a 0.9 percent rate, while services increased at a modest 2.3 percent rate after growing at a 1.6 percent rate in the fourth quarter. These are very normal pre-pandemic growth rates for services, suggesting we will not see a big post-pandemic surge.

Saving Rate Rises to 4.8 Percent in the First Quarter

The saving rate rose to 4.8 percent in the first quarter, up from 3.2 percent in the third quarter of 2022 and 4.0 percent in the fourth quarter. This increase is primarily because people are paying less in taxes, which raises disposable income. The 4.8 percent saving rate is lower than the pre-pandemic average, which was over 7.0 percent, but it is likely to rise in future quarters if vehicle sales fall back to more normal levels. There seems to be little basis for fears that people are consuming excessively and running down their pandemic savings.

Decline in Residential Investment Slows

Residential investment fell at double-digit rates in the last three quarters of 2022. This drop was partly driven by a collapse in mortgage refinancing, which had been booming with the low pandemic interest rates. Now that refinancing has virtually stopped, it has no further room to fall. While housing construction has fallen, the number of units under construction is still as high as when the Fed began raising rates last year. This number is due to the large backlog of unfinished houses due to supply chain problems. Construction will slow further as these get finished over the year, but the big declines are largely behind us.

Strong Structure Investment Keeps Non-Residential Investment Positive

Non-residential investment grew at a 0.7 percent annual rate in the quarter. This growth was primarily due to an 11.2 percent rise in structure investment. This rise follows an increase of 15.8 percent in the fourth quarter of last year, after six consecutive quarters of decline. The main factor in the jump in structure investment is manufacturing structures. Investment in factories in the first quarter was 40.5 percent higher than in the third quarter of 2022.

Equipment investment fell at a 7.3 percent rate in the quarter. Most of the drop was due to a fall in spending on aircraft and farm equipment. Investment in farm equipment in the first quarter was down by 25.7 percent from the third quarter level.

Investment in intellectual products grew at a modest 3.8 percent, which is down from 9.7 percent and 8.8 percent rates in 2021 and 2022, respectively. This sector is seeing mixed pressures, as many traditional media and social media companies cut back after major expansions during the pandemic. On the other side, the race for AI will be forcing many companies to increase investment. If we see any declines in this component, they are unlikely to be large.

Trade is Small Positive, as Export Growth Outpaces Imports

Trade contributed 0.11 pp to the quarter’s growth, as a 4.8 percent rise in exports more than offset the impact of a 2.9 percent rise in imports. Goods exports actually rose at a more rapid 10.0 percent, as there was an unusual decline of 5.5 percent in service exports. After expanding rapidly during the pandemic, the trade deficit has fallen back to roughly its pre-pandemic share of GDP. It will not likely be a major factor in GDP growth going forward.

Government Spending Adds 0.81 Percentage Points to Growth in Quarter

Overall, government spending rose at a 4.7 percent annual rate, with federal spending rising at a 7.8 percent rate and state and local spending rising at a 2.9 percent rate. Non-defense federal spending grew at a 10.3 percent rate in the quarter. The strong growth in non-defense federal spending is likely somewhat of an anomaly, as this component is often erratic, especially since the pandemic. It fell by 9.2 percent in the second quarter, after dropping at a 1.1 percent rate in the first quarter.

PCE Deflator Rises at 4.2 Percent Annual Rate

The price indices came in largely as expected, with the overall personal consumption expenditure deflator rising at a 4.2 percent rate and the core index rising at 4.9 percent rate. One encouraging item is a 1.2 percent decline in import prices, the third consecutive quarter of decline. Import prices had risen 13.5 percent and 13.2 percent in the first and second quarters of last year. (These prices do not include shipping costs.) Since imports include both finished consumer goods, like clothes and cars, and also inputs to items produced here, the turnaround should be a good sign for future inflation.

Economy Still Looks Very Healthy

In the spite of the widespread concerns about a looming recession, it is difficult to see the basis for one in the first quarter GDP data. Housing is likely to continue to edge lower over the course of 2023, but the big falls are likely behind us. There is a similar story with non-residential construction, with the surge in factory construction turning this category positive. Consumer spending is growing at a healthy pace, with little obvious reason to expect a reversal any time soon. The fallout from the banking crisis is a big uncertainty, but otherwise this is a very positive picture.

The Center for Economic and Policy Research (CEPR) was established in 1999 to promote democratic debate on the most important economic and social issues that affect people's lives. In order for citizens to effectively exercise their voices in a democracy, they should be informed about the problems and choices that they face. CEPR is committed to presenting issues in an accurate and understandable manner, so that the public is better prepared to choose among the various policy options.

(202) 293-5380