SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

When jobs are plentiful and business profits soar, that means good news for federal tax revenues. At least, that’s how it’s supposed to work.

For 15 years after the Tax Reform Act of 1986 went into effect, that’s exactly what happened: Changes in the U.S. unemployment rate were a strong predictor of changes in our federal tax revenues as a percent of the GDP; a drop in the unemployment rate caused revenues as a percent of GDP to increase. But since the beginning of the 21st century, a series of tax cuts under presidents George W. Bush and Donald Trump have shattered the link between tax revenues and employment. Revenues as a percent of GDP dropped significantly, and now they no longer grow much when the economy strengthens.

After news that the federal deficit grew despite a strong economy, amid rising interest rates, there are renewed fears about the nation’s fiscal outlook. With these fears typically come calls to reduce spending. But the U.S. doesn’t have a spending problem; it has a revenue problem caused by tax cuts.

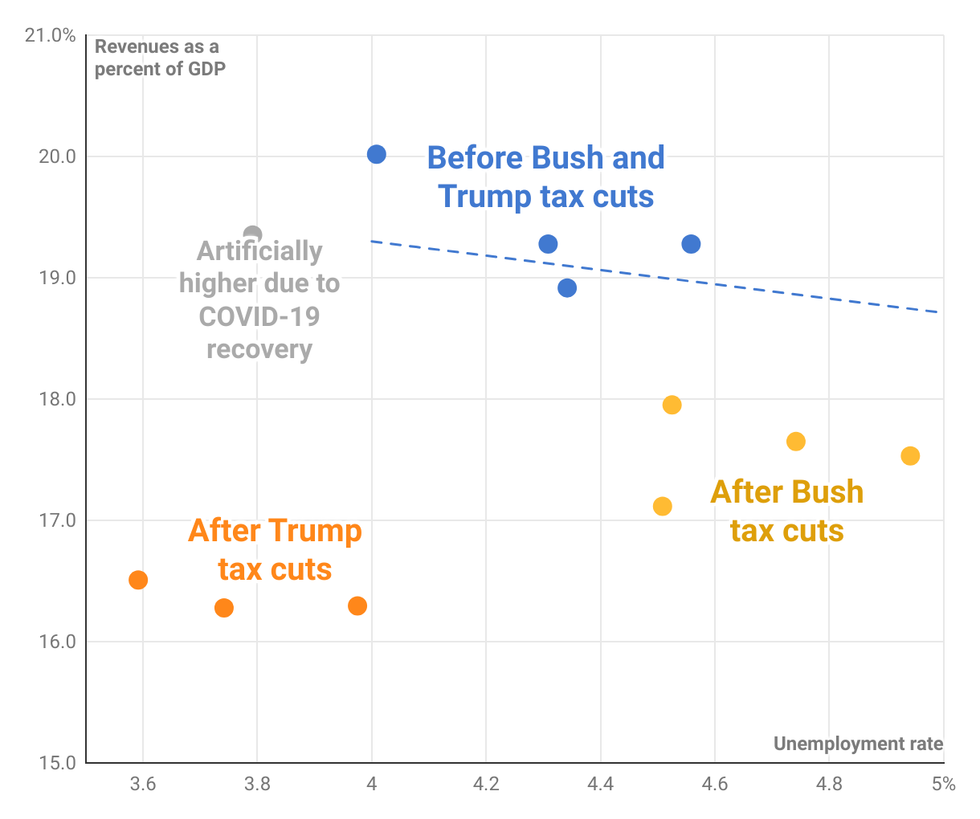

The Bush and Trump tax cuts broke our modern tax structure: Revenues are significantly lower and no longer grow much with the economy

(Chart: Center for American Progress)

(Chart: Center for American Progress)

Between 1995 and 2000, the unemployment rate fell from 5.6% to 4.0%, and revenues rose from 17.9% to 20.0% of GDP—the equivalent of taking in an additional $600 billion per year after adjusting for the size of the economy. When the unemployment rate fell a similar amount between 2015 and 2019, going from 5.4% to 3.7%, revenues dropped from 17.9% of GDP to 16.3%—the equivalent of taking in $450 billion less per year after adjusting for the size of the economy.

Why did this happen? Because during that same time, the Bush tax cuts, their bipartisan extensions, and later the Trump tax cuts slashed taxes, significantly lowering overall revenue. Importantly, a disproportionate share of the benefits from these cuts accrued to very rich Americans, profitable corporations and wealthy heirs.

This newfound pattern of low revenues even in times of high employment has persisted up to the present day. In fiscal year 2023—which just ended September 30—the unemployment rate averaged 3.6%, the lowest since 1969. However, because of these large tax cuts, revenues were a paltry 16.5% of GDP.

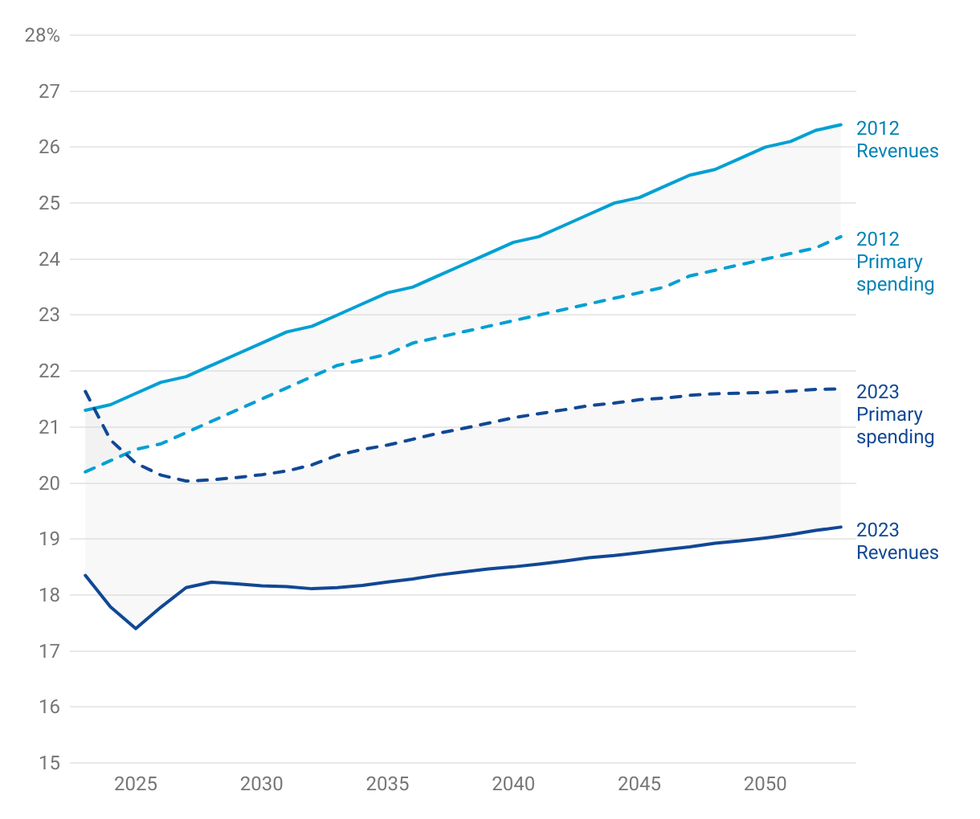

These lower revenues have a profound impact on the finances of the nation. Prior to the tax cuts being enacted, the Congressional Budget Office projected long-term stability of the debt-to-GDP ratio. Yes, the CBO projected rising spending driven by Medicare, Medicaid and Social Security. But the agency also projected that revenues would be able to keep up indefinitely without any additional tax increases, due to real wage gains leading to higher revenues. Now, however, the CBO projects that debt is on track to rise as a percent of GDP indefinitely, with revenues now significantly lower and no longer projected to match primary (noninterest) program costs.

Two points explain this. The first involves a concept called the fiscal gap, which measures how much primary deficit reduction is required to stabilize the debt-to-GDP ratio. The 30-year fiscal gap is smaller than the size of the Bush tax cuts, their extensions and the Trump tax cuts under current law over the next 30 years. Therefore, mathematically and unequivocally, without those tax cuts, the debt ratio would be declining, not rising.

Second, even though the debt ratio is rising, spending can’t be blamed. The CBO’s 2012 long-term budget outlook was the last time debt was projected to decline indefinitely—because that projection was made before the Bush tax cuts were largely permanently extended. And relative to the CBO’s 2012 projection, current projections of program costs are down, not up. In short, if you were trying to explain how we got from the CBO’s 2012 projection of a declining debt ratio to its current projections of a rising debt ratio, changes in spending have lowered the future debt path, but revenues have declined significantly more than spending. Changes in revenues are therefore entirely responsible for going from a declining debt ratio to an ever-growing debt ratio.

Both revenues and spending are lower than earlier projections, meaning low revenues are responsible for persistent primary deficits

(Chart: Center for American Progress)

(Chart: Center for American Progress)

The first step in effecting change is proper diagnosis. Those who look to blame spending to close the primary deficit are looking in the wrong place. If not for the regressive tax cuts initiated under presidents Bush and Trump, we would have been looking at a stable debt-to-GDP ratio. Any discussion of how to change our fiscal path should focus first on generating additional revenue lost to these tax cuts.

When jobs are plentiful and business profits soar, that means good news for federal tax revenues. At least, that’s how it’s supposed to work.

For 15 years after the Tax Reform Act of 1986 went into effect, that’s exactly what happened: Changes in the U.S. unemployment rate were a strong predictor of changes in our federal tax revenues as a percent of the GDP; a drop in the unemployment rate caused revenues as a percent of GDP to increase. But since the beginning of the 21st century, a series of tax cuts under presidents George W. Bush and Donald Trump have shattered the link between tax revenues and employment. Revenues as a percent of GDP dropped significantly, and now they no longer grow much when the economy strengthens.

After news that the federal deficit grew despite a strong economy, amid rising interest rates, there are renewed fears about the nation’s fiscal outlook. With these fears typically come calls to reduce spending. But the U.S. doesn’t have a spending problem; it has a revenue problem caused by tax cuts.

The Bush and Trump tax cuts broke our modern tax structure: Revenues are significantly lower and no longer grow much with the economy

(Chart: Center for American Progress)

Between 1995 and 2000, the unemployment rate fell from 5.6% to 4.0%, and revenues rose from 17.9% to 20.0% of GDP—the equivalent of taking in an additional $600 billion per year after adjusting for the size of the economy. When the unemployment rate fell a similar amount between 2015 and 2019, going from 5.4% to 3.7%, revenues dropped from 17.9% of GDP to 16.3%—the equivalent of taking in $450 billion less per year after adjusting for the size of the economy.

Why did this happen? Because during that same time, the Bush tax cuts, their bipartisan extensions, and later the Trump tax cuts slashed taxes, significantly lowering overall revenue. Importantly, a disproportionate share of the benefits from these cuts accrued to very rich Americans, profitable corporations and wealthy heirs.

This newfound pattern of low revenues even in times of high employment has persisted up to the present day. In fiscal year 2023—which just ended September 30—the unemployment rate averaged 3.6%, the lowest since 1969. However, because of these large tax cuts, revenues were a paltry 16.5% of GDP.

These lower revenues have a profound impact on the finances of the nation. Prior to the tax cuts being enacted, the Congressional Budget Office projected long-term stability of the debt-to-GDP ratio. Yes, the CBO projected rising spending driven by Medicare, Medicaid and Social Security. But the agency also projected that revenues would be able to keep up indefinitely without any additional tax increases, due to real wage gains leading to higher revenues. Now, however, the CBO projects that debt is on track to rise as a percent of GDP indefinitely, with revenues now significantly lower and no longer projected to match primary (noninterest) program costs.

Two points explain this. The first involves a concept called the fiscal gap, which measures how much primary deficit reduction is required to stabilize the debt-to-GDP ratio. The 30-year fiscal gap is smaller than the size of the Bush tax cuts, their extensions and the Trump tax cuts under current law over the next 30 years. Therefore, mathematically and unequivocally, without those tax cuts, the debt ratio would be declining, not rising.

Second, even though the debt ratio is rising, spending can’t be blamed. The CBO’s 2012 long-term budget outlook was the last time debt was projected to decline indefinitely—because that projection was made before the Bush tax cuts were largely permanently extended. And relative to the CBO’s 2012 projection, current projections of program costs are down, not up. In short, if you were trying to explain how we got from the CBO’s 2012 projection of a declining debt ratio to its current projections of a rising debt ratio, changes in spending have lowered the future debt path, but revenues have declined significantly more than spending. Changes in revenues are therefore entirely responsible for going from a declining debt ratio to an ever-growing debt ratio.

Both revenues and spending are lower than earlier projections, meaning low revenues are responsible for persistent primary deficits

(Chart: Center for American Progress)

The first step in effecting change is proper diagnosis. Those who look to blame spending to close the primary deficit are looking in the wrong place. If not for the regressive tax cuts initiated under presidents Bush and Trump, we would have been looking at a stable debt-to-GDP ratio. Any discussion of how to change our fiscal path should focus first on generating additional revenue lost to these tax cuts.

When jobs are plentiful and business profits soar, that means good news for federal tax revenues. At least, that’s how it’s supposed to work.

For 15 years after the Tax Reform Act of 1986 went into effect, that’s exactly what happened: Changes in the U.S. unemployment rate were a strong predictor of changes in our federal tax revenues as a percent of the GDP; a drop in the unemployment rate caused revenues as a percent of GDP to increase. But since the beginning of the 21st century, a series of tax cuts under presidents George W. Bush and Donald Trump have shattered the link between tax revenues and employment. Revenues as a percent of GDP dropped significantly, and now they no longer grow much when the economy strengthens.

After news that the federal deficit grew despite a strong economy, amid rising interest rates, there are renewed fears about the nation’s fiscal outlook. With these fears typically come calls to reduce spending. But the U.S. doesn’t have a spending problem; it has a revenue problem caused by tax cuts.

The Bush and Trump tax cuts broke our modern tax structure: Revenues are significantly lower and no longer grow much with the economy

(Chart: Center for American Progress)

Between 1995 and 2000, the unemployment rate fell from 5.6% to 4.0%, and revenues rose from 17.9% to 20.0% of GDP—the equivalent of taking in an additional $600 billion per year after adjusting for the size of the economy. When the unemployment rate fell a similar amount between 2015 and 2019, going from 5.4% to 3.7%, revenues dropped from 17.9% of GDP to 16.3%—the equivalent of taking in $450 billion less per year after adjusting for the size of the economy.

Why did this happen? Because during that same time, the Bush tax cuts, their bipartisan extensions, and later the Trump tax cuts slashed taxes, significantly lowering overall revenue. Importantly, a disproportionate share of the benefits from these cuts accrued to very rich Americans, profitable corporations and wealthy heirs.

This newfound pattern of low revenues even in times of high employment has persisted up to the present day. In fiscal year 2023—which just ended September 30—the unemployment rate averaged 3.6%, the lowest since 1969. However, because of these large tax cuts, revenues were a paltry 16.5% of GDP.

These lower revenues have a profound impact on the finances of the nation. Prior to the tax cuts being enacted, the Congressional Budget Office projected long-term stability of the debt-to-GDP ratio. Yes, the CBO projected rising spending driven by Medicare, Medicaid and Social Security. But the agency also projected that revenues would be able to keep up indefinitely without any additional tax increases, due to real wage gains leading to higher revenues. Now, however, the CBO projects that debt is on track to rise as a percent of GDP indefinitely, with revenues now significantly lower and no longer projected to match primary (noninterest) program costs.

Two points explain this. The first involves a concept called the fiscal gap, which measures how much primary deficit reduction is required to stabilize the debt-to-GDP ratio. The 30-year fiscal gap is smaller than the size of the Bush tax cuts, their extensions and the Trump tax cuts under current law over the next 30 years. Therefore, mathematically and unequivocally, without those tax cuts, the debt ratio would be declining, not rising.

Second, even though the debt ratio is rising, spending can’t be blamed. The CBO’s 2012 long-term budget outlook was the last time debt was projected to decline indefinitely—because that projection was made before the Bush tax cuts were largely permanently extended. And relative to the CBO’s 2012 projection, current projections of program costs are down, not up. In short, if you were trying to explain how we got from the CBO’s 2012 projection of a declining debt ratio to its current projections of a rising debt ratio, changes in spending have lowered the future debt path, but revenues have declined significantly more than spending. Changes in revenues are therefore entirely responsible for going from a declining debt ratio to an ever-growing debt ratio.

Both revenues and spending are lower than earlier projections, meaning low revenues are responsible for persistent primary deficits

(Chart: Center for American Progress)

The first step in effecting change is proper diagnosis. Those who look to blame spending to close the primary deficit are looking in the wrong place. If not for the regressive tax cuts initiated under presidents Bush and Trump, we would have been looking at a stable debt-to-GDP ratio. Any discussion of how to change our fiscal path should focus first on generating additional revenue lost to these tax cuts.