SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Editor's note: On Thursday evening, in a 63-36 final vote that included 46 members of the Democratic caucus in the yea column, the U.S. Senate approved the Fiscal Responsibility Act of 2023, sending the bill—already approved by the U.S. House—to President Joe Biden's desk for signature.

For months the White House proclaimed that it would not negotiate with Republicans over spending cuts in exchange for raising the debt ceiling. It insisted that it would accept only a clean lift of the borrowing limits. Then a few weeks ago, as prospects of default on the federal debt increasingly weighed on financial markets, the administration commenced negotiating.

Reactions were all over the political map. Some observers, mostly Republicans and what the press keeps hailing as “moderate” Democrats, professed happy surprise. Others were wary. Far-right Republicans doubted the possibilities for any deal they could accept.

Progressive Democrats, by contrast, recalled the many cases in which their leaders horse-traded with Republicans over spending programs while laying off tax cuts. They looked back in particular to President Obama’s famous attempt at a “grand bargain” with Republicans in 2011 – an episode in which then Vice President Joe Biden played a key role. That ratified major Bush-era tax cuts and severely impacted federal spending for years, likely contributing to the voter disaffection with Democrats that became dramatically evident in 2016.

Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The way the President chose to negotiate this time did nothing to ease such fears. A New York Times editorial observed that “Democrats could have voted to eliminate the debt ceiling between the fall elections and January, when Republicans took control of the House, or they could have voted to provide the government with sufficient borrowing capacity until the next congressional elections in 2024. Instead, they chose this confrontation. Mr. Biden last fall labeled proposals to eliminate the debt ceiling ‘irresponsible.’ Other Democrats appeared to relish the politics of a fight. Now they are facing the consequences, which will most likely include the partial reversal of legislative victories won during Mr. Biden’s first two years.”

In public the White House conducted talks only with House Speaker McCarthy, leaving out Democrats in both houses. Meantime Senate Majority Leader Charles Schumer, whose political career has been coterminous with New York City’s ascent as the capital of world finance, made noises about wanting a bipartisan deal. He also ostentatiously failed to match Speaker McCarthy’s purely-for-show vote on a debt ceiling package with a Democratic counterpart that the public and the press could easily compare.

Whatever one thinks of their legal merits, it was also odd that Democratic leaders, including the President, played down prospects for cutting off outlandish Republican demands by resorting to unconventional ways out of the crisis, such as minting the fabled trillion-dollar platinum coin or invoking the 14th amendment.

No wonder Paul Krugman voiced skepticism about what was behind the White House’s calculations. “More and more it looks as if there never was a strategy beyond wishful thinking. I hope that I’m wrong about this…But right now I have a sick feeling about all of this. What were they thinking? How can they have been caught so off-guard by something that everyone who’s paying attention saw coming?”

The answer, we fear, is not edifying. The White House was not caught off guard. Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The reason is simple: The dominating fact about American politics is its money-driven character. In our world, both major political parties are first of all bank accounts, which have to be filled for anything to happen. Voters can drive politics, but not easily. Unless they are prepared to invest very substantial time and effort into making the system work or organizations that they control will – such as unions or genuine grassroots political organizations – only political appeals that can be financed go live in the system, unless (of course) as helpful diversions.

The result is what we term the “linear model” of U.S. congressional elections: to a stunning degree outcomes of elections between major party candidates are directly proportional to the amounts of money each raises and spends. This dependence is a feature, not a bug; as we have quite elaborately shown, you can rule out the possibility that this relationship arises because money is mostly just following public opinion.[1]

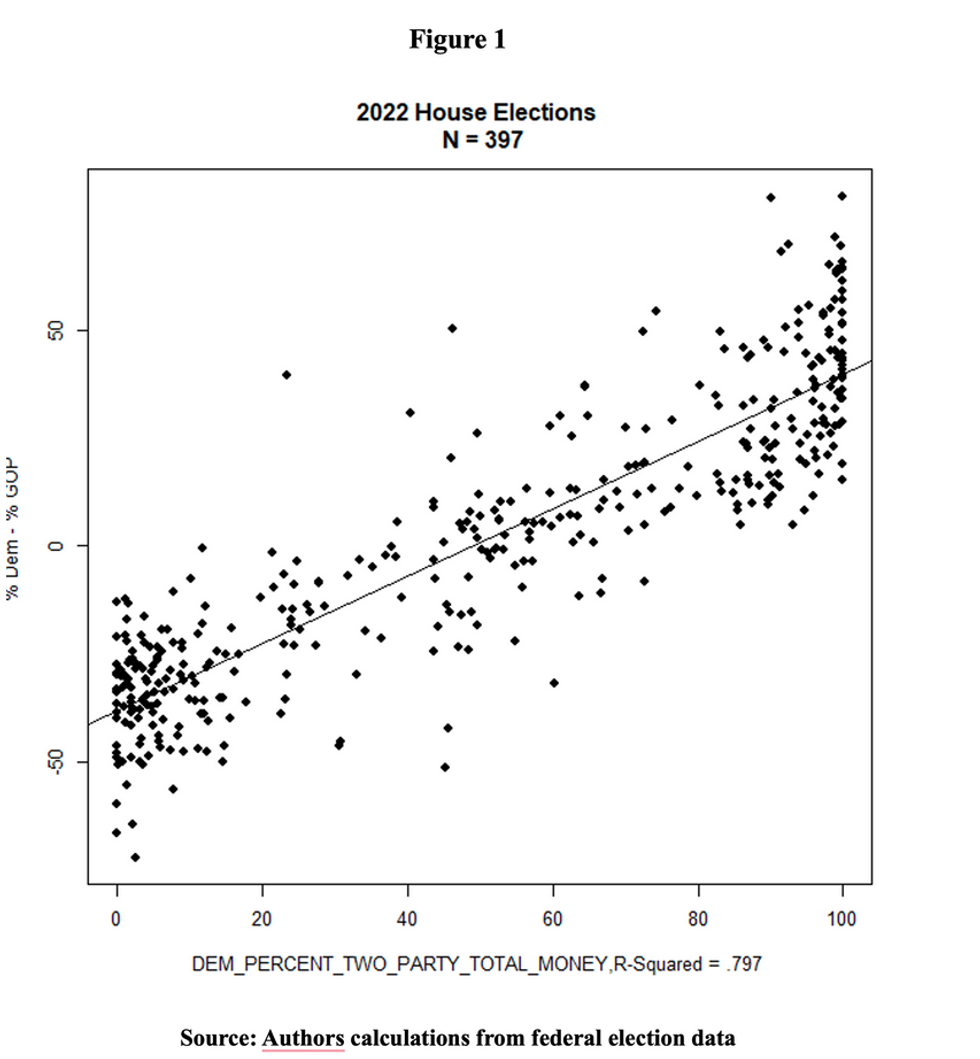

Our graphs for money and politics in the House and Senate elections of 2022 look like all the other elections for which we have data.

First, the House.

The straight line shows that the percentage of money the Democratic candidates spend strongly predicts the percentage of the two party vote they receive. As we have explained many times before, the model covers only cases in which candidates of the two opposing major parties face each other. This is the norm, but the condition does exclude a few, so the total number of races is slightly less than 100%.[2]

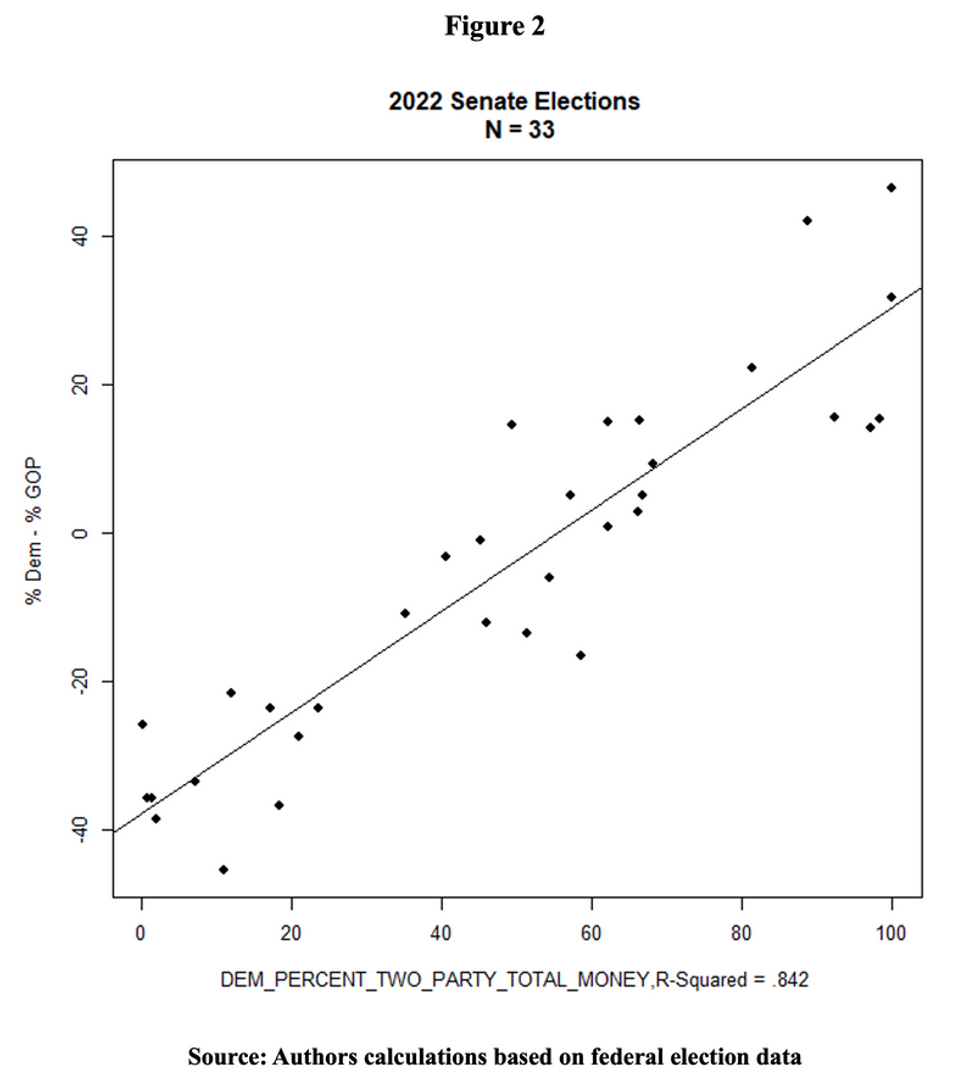

In 2022, the Senate displayed precisely the same pattern to a degree that is, well, unusual, even for American politics. Yes, the number of Senate races is much smaller, so the results are less reliable. But the startingly tight fit should be an embarrassment for anyone concerned with democratic elections.[3]

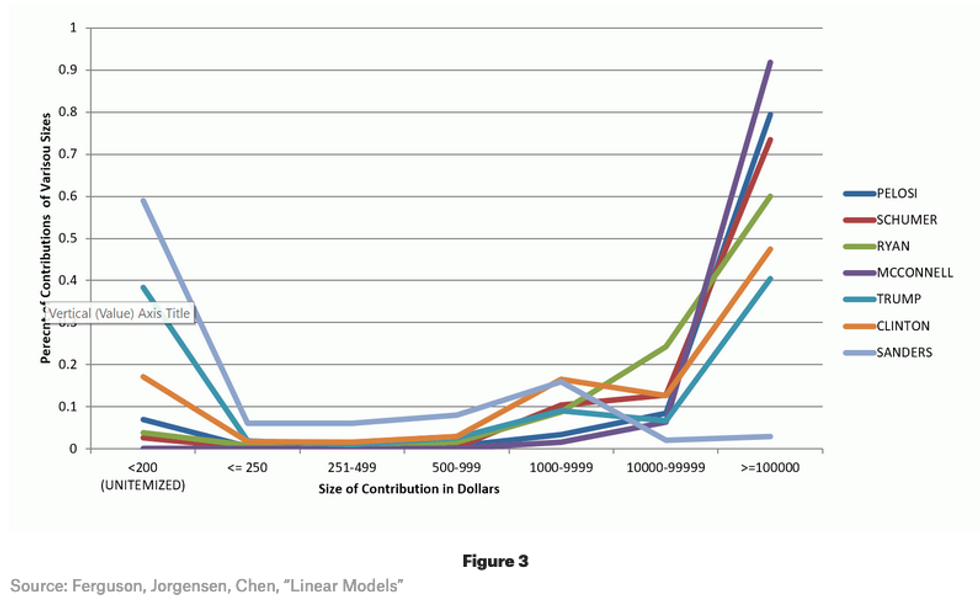

Most of this money comes from wealthy donors and companies. It does not come from ordinary Americans. To why this is important for the borrowing limit debate it is helpful to look once more at a figure we have used before. This plots the percentage of large and small donations for key presidential candidates in 2016 and the Congressional leadership for that year.

The pattern it shows is unmistakable: one candidate, Senator Bernie Sanders, received 60% of his funds from small donors while garnering essentially no donations from rich Americans. The composition of Donald Trump’s money shows a striking shape we have often commented up: a barbell in which small donors do contribute some important money, but with most of his funds coming from the very richest Americans. By contrast, the lion’s share of everyone else’s funds come heavily from the superrich, including Hillary Clinton and the entire Congressional leadership, with Mitch McConnell a particularly striking case.

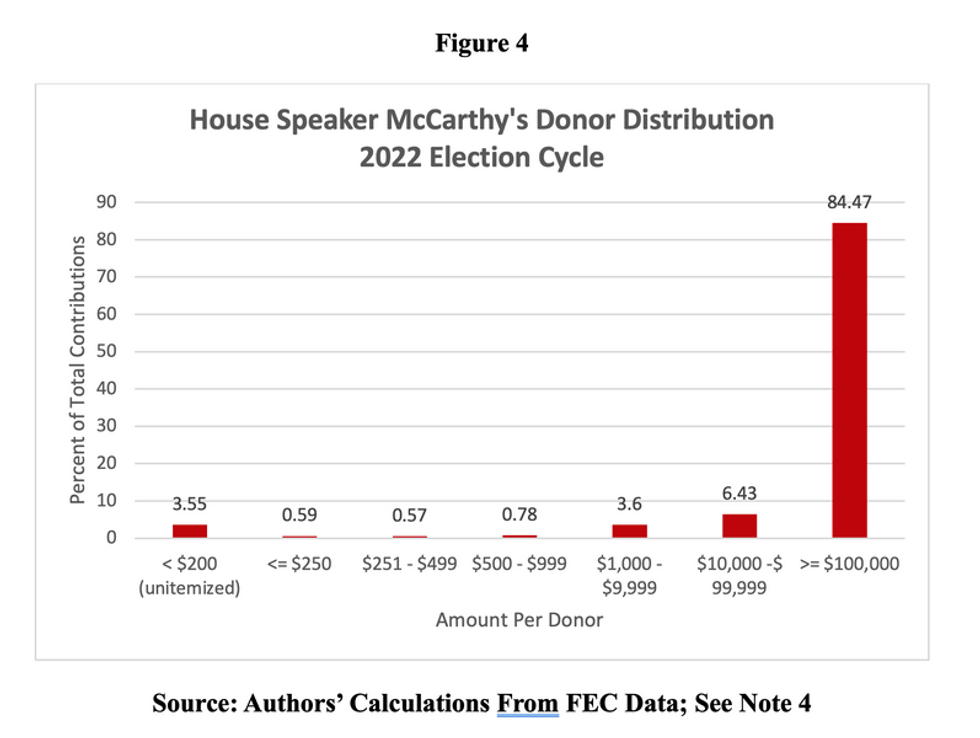

We are in the midst of calculating equivalent figures for 2020 and 2022; we do not believe they changed in any essential way. Sanders is still unpopular with big donors, Biden and Trump both depended in 2020 on big donations and so did Congressional leaders. In the case of McCarthy, however, we can show this is true to a preposterous extent.[4]

What all this implies for the borrowing limit debate is easily summarized. First, recall the fate of President Biden’s very modest proposals for new taxes as he entered office. While in many cases applauding his program, not a single major business organization in the United States was willing to support his suggestions.

At the time some commentators complained that these stances were inconsistent. But of course in the world of the investment theory of political parties, there is no contradiction between favoring major investments in defense or even climate change, but also wanting ordinary Americans to pay for them. That’s just money politics as usual.

Now the President is running for a second term. His fundraisers openly declare that the campaign intends to raise more than a billion dollars. In recent presidential elections, contributions from labor union amount to about 6 or 7% of total political spending. Money in the amounts the Biden campaign seeks can come only from one place: from the superrich and very affluent Americans. And in a Congress so dependent on money flows, relatively few representatives in either party are likely to do much more than posture when it comes to raising taxes. For Democrats in particular, the advantages of first actually passing programs, then standing back and reluctantly sustaining votes to take them back are a dream come true for squaring big money politics with folk appeal. That is the real reason Democratic party leaders go along with the debt ceiling ritual.

This is not to say that the compromise package that is now making headlines is guaranteed to have smooth sailing. Questions about the future policy on permits for oil and gas and green energy access to the electrical grid are already sparking protests. The Inflation Control Act marked a shift in the President’s priorities from not only promoting sustainability but also renewing the US role as a global exporter of natural gas. The debt ceiling accord reflects the same dual emphases. The interests in play here are immensely powerful on both sides. Some might balk or hold out for more. But that issue has no bearing on the cardinal point: that right now agreeing to limit federal borrowing while going through the motions on raising taxes will pay off handsomely for Democrats if hardly for many of their voters.

Editor's note: On Thursday evening, in a 63-36 final vote that included 46 members of the Democratic caucus in the yea column, the U.S. Senate approved the Fiscal Responsibility Act of 2023, sending the bill—already approved by the U.S. House—to President Joe Biden's desk for signature.

For months the White House proclaimed that it would not negotiate with Republicans over spending cuts in exchange for raising the debt ceiling. It insisted that it would accept only a clean lift of the borrowing limits. Then a few weeks ago, as prospects of default on the federal debt increasingly weighed on financial markets, the administration commenced negotiating.

Reactions were all over the political map. Some observers, mostly Republicans and what the press keeps hailing as “moderate” Democrats, professed happy surprise. Others were wary. Far-right Republicans doubted the possibilities for any deal they could accept.

Progressive Democrats, by contrast, recalled the many cases in which their leaders horse-traded with Republicans over spending programs while laying off tax cuts. They looked back in particular to President Obama’s famous attempt at a “grand bargain” with Republicans in 2011 – an episode in which then Vice President Joe Biden played a key role. That ratified major Bush-era tax cuts and severely impacted federal spending for years, likely contributing to the voter disaffection with Democrats that became dramatically evident in 2016.

Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The way the President chose to negotiate this time did nothing to ease such fears. A New York Times editorial observed that “Democrats could have voted to eliminate the debt ceiling between the fall elections and January, when Republicans took control of the House, or they could have voted to provide the government with sufficient borrowing capacity until the next congressional elections in 2024. Instead, they chose this confrontation. Mr. Biden last fall labeled proposals to eliminate the debt ceiling ‘irresponsible.’ Other Democrats appeared to relish the politics of a fight. Now they are facing the consequences, which will most likely include the partial reversal of legislative victories won during Mr. Biden’s first two years.”

In public the White House conducted talks only with House Speaker McCarthy, leaving out Democrats in both houses. Meantime Senate Majority Leader Charles Schumer, whose political career has been coterminous with New York City’s ascent as the capital of world finance, made noises about wanting a bipartisan deal. He also ostentatiously failed to match Speaker McCarthy’s purely-for-show vote on a debt ceiling package with a Democratic counterpart that the public and the press could easily compare.

Whatever one thinks of their legal merits, it was also odd that Democratic leaders, including the President, played down prospects for cutting off outlandish Republican demands by resorting to unconventional ways out of the crisis, such as minting the fabled trillion-dollar platinum coin or invoking the 14th amendment.

No wonder Paul Krugman voiced skepticism about what was behind the White House’s calculations. “More and more it looks as if there never was a strategy beyond wishful thinking. I hope that I’m wrong about this…But right now I have a sick feeling about all of this. What were they thinking? How can they have been caught so off-guard by something that everyone who’s paying attention saw coming?”

The answer, we fear, is not edifying. The White House was not caught off guard. Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The reason is simple: The dominating fact about American politics is its money-driven character. In our world, both major political parties are first of all bank accounts, which have to be filled for anything to happen. Voters can drive politics, but not easily. Unless they are prepared to invest very substantial time and effort into making the system work or organizations that they control will – such as unions or genuine grassroots political organizations – only political appeals that can be financed go live in the system, unless (of course) as helpful diversions.

The result is what we term the “linear model” of U.S. congressional elections: to a stunning degree outcomes of elections between major party candidates are directly proportional to the amounts of money each raises and spends. This dependence is a feature, not a bug; as we have quite elaborately shown, you can rule out the possibility that this relationship arises because money is mostly just following public opinion.[1]

Our graphs for money and politics in the House and Senate elections of 2022 look like all the other elections for which we have data.

First, the House.

The straight line shows that the percentage of money the Democratic candidates spend strongly predicts the percentage of the two party vote they receive. As we have explained many times before, the model covers only cases in which candidates of the two opposing major parties face each other. This is the norm, but the condition does exclude a few, so the total number of races is slightly less than 100%.[2]

In 2022, the Senate displayed precisely the same pattern to a degree that is, well, unusual, even for American politics. Yes, the number of Senate races is much smaller, so the results are less reliable. But the startingly tight fit should be an embarrassment for anyone concerned with democratic elections.[3]

Most of this money comes from wealthy donors and companies. It does not come from ordinary Americans. To why this is important for the borrowing limit debate it is helpful to look once more at a figure we have used before. This plots the percentage of large and small donations for key presidential candidates in 2016 and the Congressional leadership for that year.

The pattern it shows is unmistakable: one candidate, Senator Bernie Sanders, received 60% of his funds from small donors while garnering essentially no donations from rich Americans. The composition of Donald Trump’s money shows a striking shape we have often commented up: a barbell in which small donors do contribute some important money, but with most of his funds coming from the very richest Americans. By contrast, the lion’s share of everyone else’s funds come heavily from the superrich, including Hillary Clinton and the entire Congressional leadership, with Mitch McConnell a particularly striking case.

We are in the midst of calculating equivalent figures for 2020 and 2022; we do not believe they changed in any essential way. Sanders is still unpopular with big donors, Biden and Trump both depended in 2020 on big donations and so did Congressional leaders. In the case of McCarthy, however, we can show this is true to a preposterous extent.[4]

What all this implies for the borrowing limit debate is easily summarized. First, recall the fate of President Biden’s very modest proposals for new taxes as he entered office. While in many cases applauding his program, not a single major business organization in the United States was willing to support his suggestions.

At the time some commentators complained that these stances were inconsistent. But of course in the world of the investment theory of political parties, there is no contradiction between favoring major investments in defense or even climate change, but also wanting ordinary Americans to pay for them. That’s just money politics as usual.

Now the President is running for a second term. His fundraisers openly declare that the campaign intends to raise more than a billion dollars. In recent presidential elections, contributions from labor union amount to about 6 or 7% of total political spending. Money in the amounts the Biden campaign seeks can come only from one place: from the superrich and very affluent Americans. And in a Congress so dependent on money flows, relatively few representatives in either party are likely to do much more than posture when it comes to raising taxes. For Democrats in particular, the advantages of first actually passing programs, then standing back and reluctantly sustaining votes to take them back are a dream come true for squaring big money politics with folk appeal. That is the real reason Democratic party leaders go along with the debt ceiling ritual.

This is not to say that the compromise package that is now making headlines is guaranteed to have smooth sailing. Questions about the future policy on permits for oil and gas and green energy access to the electrical grid are already sparking protests. The Inflation Control Act marked a shift in the President’s priorities from not only promoting sustainability but also renewing the US role as a global exporter of natural gas. The debt ceiling accord reflects the same dual emphases. The interests in play here are immensely powerful on both sides. Some might balk or hold out for more. But that issue has no bearing on the cardinal point: that right now agreeing to limit federal borrowing while going through the motions on raising taxes will pay off handsomely for Democrats if hardly for many of their voters.

Editor's note: On Thursday evening, in a 63-36 final vote that included 46 members of the Democratic caucus in the yea column, the U.S. Senate approved the Fiscal Responsibility Act of 2023, sending the bill—already approved by the U.S. House—to President Joe Biden's desk for signature.

For months the White House proclaimed that it would not negotiate with Republicans over spending cuts in exchange for raising the debt ceiling. It insisted that it would accept only a clean lift of the borrowing limits. Then a few weeks ago, as prospects of default on the federal debt increasingly weighed on financial markets, the administration commenced negotiating.

Reactions were all over the political map. Some observers, mostly Republicans and what the press keeps hailing as “moderate” Democrats, professed happy surprise. Others were wary. Far-right Republicans doubted the possibilities for any deal they could accept.

Progressive Democrats, by contrast, recalled the many cases in which their leaders horse-traded with Republicans over spending programs while laying off tax cuts. They looked back in particular to President Obama’s famous attempt at a “grand bargain” with Republicans in 2011 – an episode in which then Vice President Joe Biden played a key role. That ratified major Bush-era tax cuts and severely impacted federal spending for years, likely contributing to the voter disaffection with Democrats that became dramatically evident in 2016.

Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The way the President chose to negotiate this time did nothing to ease such fears. A New York Times editorial observed that “Democrats could have voted to eliminate the debt ceiling between the fall elections and January, when Republicans took control of the House, or they could have voted to provide the government with sufficient borrowing capacity until the next congressional elections in 2024. Instead, they chose this confrontation. Mr. Biden last fall labeled proposals to eliminate the debt ceiling ‘irresponsible.’ Other Democrats appeared to relish the politics of a fight. Now they are facing the consequences, which will most likely include the partial reversal of legislative victories won during Mr. Biden’s first two years.”

In public the White House conducted talks only with House Speaker McCarthy, leaving out Democrats in both houses. Meantime Senate Majority Leader Charles Schumer, whose political career has been coterminous with New York City’s ascent as the capital of world finance, made noises about wanting a bipartisan deal. He also ostentatiously failed to match Speaker McCarthy’s purely-for-show vote on a debt ceiling package with a Democratic counterpart that the public and the press could easily compare.

Whatever one thinks of their legal merits, it was also odd that Democratic leaders, including the President, played down prospects for cutting off outlandish Republican demands by resorting to unconventional ways out of the crisis, such as minting the fabled trillion-dollar platinum coin or invoking the 14th amendment.

No wonder Paul Krugman voiced skepticism about what was behind the White House’s calculations. “More and more it looks as if there never was a strategy beyond wishful thinking. I hope that I’m wrong about this…But right now I have a sick feeling about all of this. What were they thinking? How can they have been caught so off-guard by something that everyone who’s paying attention saw coming?”

The answer, we fear, is not edifying. The White House was not caught off guard. Like climate disaster, the crypto meltdowns, and the tremors now coursing through the American financial system, the high noon showdown between Republicans and Democrats over the debt ceiling was pre-programmed from the start.

The reason is simple: The dominating fact about American politics is its money-driven character. In our world, both major political parties are first of all bank accounts, which have to be filled for anything to happen. Voters can drive politics, but not easily. Unless they are prepared to invest very substantial time and effort into making the system work or organizations that they control will – such as unions or genuine grassroots political organizations – only political appeals that can be financed go live in the system, unless (of course) as helpful diversions.

The result is what we term the “linear model” of U.S. congressional elections: to a stunning degree outcomes of elections between major party candidates are directly proportional to the amounts of money each raises and spends. This dependence is a feature, not a bug; as we have quite elaborately shown, you can rule out the possibility that this relationship arises because money is mostly just following public opinion.[1]

Our graphs for money and politics in the House and Senate elections of 2022 look like all the other elections for which we have data.

First, the House.

The straight line shows that the percentage of money the Democratic candidates spend strongly predicts the percentage of the two party vote they receive. As we have explained many times before, the model covers only cases in which candidates of the two opposing major parties face each other. This is the norm, but the condition does exclude a few, so the total number of races is slightly less than 100%.[2]

In 2022, the Senate displayed precisely the same pattern to a degree that is, well, unusual, even for American politics. Yes, the number of Senate races is much smaller, so the results are less reliable. But the startingly tight fit should be an embarrassment for anyone concerned with democratic elections.[3]

Most of this money comes from wealthy donors and companies. It does not come from ordinary Americans. To why this is important for the borrowing limit debate it is helpful to look once more at a figure we have used before. This plots the percentage of large and small donations for key presidential candidates in 2016 and the Congressional leadership for that year.

The pattern it shows is unmistakable: one candidate, Senator Bernie Sanders, received 60% of his funds from small donors while garnering essentially no donations from rich Americans. The composition of Donald Trump’s money shows a striking shape we have often commented up: a barbell in which small donors do contribute some important money, but with most of his funds coming from the very richest Americans. By contrast, the lion’s share of everyone else’s funds come heavily from the superrich, including Hillary Clinton and the entire Congressional leadership, with Mitch McConnell a particularly striking case.

We are in the midst of calculating equivalent figures for 2020 and 2022; we do not believe they changed in any essential way. Sanders is still unpopular with big donors, Biden and Trump both depended in 2020 on big donations and so did Congressional leaders. In the case of McCarthy, however, we can show this is true to a preposterous extent.[4]

What all this implies for the borrowing limit debate is easily summarized. First, recall the fate of President Biden’s very modest proposals for new taxes as he entered office. While in many cases applauding his program, not a single major business organization in the United States was willing to support his suggestions.

At the time some commentators complained that these stances were inconsistent. But of course in the world of the investment theory of political parties, there is no contradiction between favoring major investments in defense or even climate change, but also wanting ordinary Americans to pay for them. That’s just money politics as usual.

Now the President is running for a second term. His fundraisers openly declare that the campaign intends to raise more than a billion dollars. In recent presidential elections, contributions from labor union amount to about 6 or 7% of total political spending. Money in the amounts the Biden campaign seeks can come only from one place: from the superrich and very affluent Americans. And in a Congress so dependent on money flows, relatively few representatives in either party are likely to do much more than posture when it comes to raising taxes. For Democrats in particular, the advantages of first actually passing programs, then standing back and reluctantly sustaining votes to take them back are a dream come true for squaring big money politics with folk appeal. That is the real reason Democratic party leaders go along with the debt ceiling ritual.

This is not to say that the compromise package that is now making headlines is guaranteed to have smooth sailing. Questions about the future policy on permits for oil and gas and green energy access to the electrical grid are already sparking protests. The Inflation Control Act marked a shift in the President’s priorities from not only promoting sustainability but also renewing the US role as a global exporter of natural gas. The debt ceiling accord reflects the same dual emphases. The interests in play here are immensely powerful on both sides. Some might balk or hold out for more. But that issue has no bearing on the cardinal point: that right now agreeing to limit federal borrowing while going through the motions on raising taxes will pay off handsomely for Democrats if hardly for many of their voters.