SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

The Los Angeles area began this year with some of the worst wildfires in its history. Dozens of people were killed and 200,000 were displaced. About 40,000 acres and 12,300 structures, including houses, were burned. The city endured immense emotional and physical damage. Yet, many property owners in the city find themselves with little recourse for financial compensation.

In fact, over the past five years, insurance companies like State Farm, Farmers, Chubb, Liberty Mutual, and Allstate have all refused to renew policies for innumerable homeowners in the Los Angeles area, leaving residents without adequate protection for their homes. By July of 2024, State Farm alone had dropped 1,600 clients residing in the Pacific Palisades ZIP code, where damage from the fires would be some of the worst. Soaring home insurance prices have also forced lower- and middle-income residents to make the impossible decision of refusing insurance for their homes. In the wake of the most recent fires, many are not only left devastated by the destruction of their homes and the uprooting of their lives, but they are also financially stranded in the disaster’s aftermath.

All of these horrible consequences stem from a simple rule that defines much of the home insurance industry’s dealings with the public: Increased risk means increased prices. In more disaster-prone areas, the likelihood of insurance companies having to compensate homeowners is heightened by the prevalence of destructive events, and insurance companies raise premiums to remain profitable and to ensure their financial ability to cover future losses or drop clients altogether. For instance, knowing that California is highly prone to destructive wildfires, insurance companies will deny housing coverage for people in high-risk forest fire areas to avoid paying the high cost of rebuilding thousands of homes should one occur.

As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Rising insurance prices are not isolated to one region, though. Communities across the country from Kentucky to Florida to New York are now facing the brunt end of this crisis. When hurricane Ida hit New York in 2021, damages cost one woman up to $25,000 dollars out of pocket for repairs because Liberty Mutual outright rejected them coverage. This disproportionately affects low-income communities, who will face even more struggle trying to afford to pay for damages that should have been covered by their housing insurance in the first place.

Even considering the fact that the burden often falls on people purchasing insurance for their homes, increased and intensified natural disasters fundamentally have an adverse financial effect on insurance companies by making their services more expensive, which is also often accompanied by reduced coverage. Therefore, you would think that they would address the root cause of this increase in destruction—climate change.

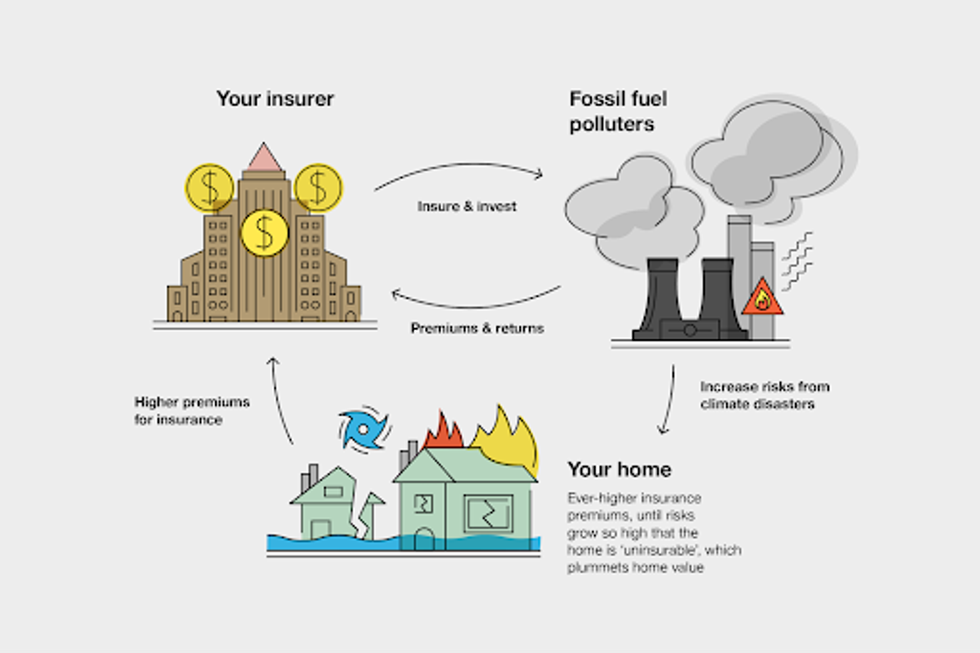

But, many don’t. Everyday, insurance companies like Chubb, Liberty Mutual, and AIG practice hypocrisy, creating a perpetual cycle that expedites climate destruction and inequality. This is accomplished through the underwriting of fossil fuel projects, which is often cheaper for these companies because it allows them to invest and insure something deemed less “risky” that, in the short-term, will make the company more money. Insurance companies continue to underwrite pipelines for transporting fossil fuels and liquefied natural gas (LNG) infrastructure that is often built nearby vulnerable communities. The domestic insurance industry has also invested $582 billion of assets collected through client’s premiums into the fossil fuel industry. Still, climate change, caused by the emission of those exact fossil fuels into the Earth’s atmosphere, further exacerbates and increases the frequency of the (not so) natural disasters that drive up insurance prices. Essentially, these companies contribute to the climate crisis through their financial choices, and then expect frontline communities to foot the bill.

(Graphic: Green America)

(Graphic: Green America)

The insurance industry is one of the key pillars of our society’s reliance on fossil fuels alongside the financial institutions that bankroll it and the government agencies that sign off on its expansion. When insurance companies provide coverage for fossil fuel extraction projects, they provide insurance so that in the case of a disaster like a spill or explosion, the extraction project is protected. Without insurance coverage, corporations simply cannot continue building the infrastructure that keeps us hooked on fossil fuels. For example, last year, when Chubb dropped the coverage from the Rio Grande LNG project, AIG stepped right in as an insurer on the initiative. As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Insurance companies, especially, know the risks of climate change and are vulnerable to its effects. A report by the asset manager Conning shows that 91% of insurance executives profess “significant” concern about the climate crisis. This makes efforts to persuade insurance companies on matters of climate particularly salient and realistic during these times—especially when the public wants change. According to one study, 78% of U.S. voters are at least somewhat concerned about rising property insurance costs and 67% percent are concerned about extreme weather events. Most importantly, the vast majority of the population surveyed said that insurance executives are to blame for the aforementioned rising costs and 57% said that these costs should not be passed on to customers.

Although older generations also suffer the difficulties of accessing reliable insurance and figuring out how to pick up their lives after devastating climate disasters, Gen Z is uniquely forced to come of age without the financial expectations and infrastructure that were promised to us as part of the American economic system. Affordable mortgages and insurers that will actually cover us and provide reliable and ethical insurance now seem near-impossible to access for young people, knowing the state of our climate. This has particularly impacted Gen Z because we have grown up in a time where climate disasters are stronger, more frequent, and now something of a regular occurrence. In response to these climate events becoming normal, companies will continue to increasingly deny us housing coverage and proper insurance in hopes of saving money. This calls youth across the country to take action against the hypocrisy of these companies, calling for sustainable insurance that does not fund the fossil fuel industry.

The shift to a fossil fuel-free insurance industry will not be easy, but it is now, more than ever, a necessary step toward ensuring the common good. It is, in fact, the only ethical option on behalf of corporations that are meant to protect people’s livelihoods. As youth, we demand immediate action from the individuals and corporations in power, and to those who refuse to listen to us, we have one question: Who do you expect to pay your premiums in 50 years?

The Los Angeles area began this year with some of the worst wildfires in its history. Dozens of people were killed and 200,000 were displaced. About 40,000 acres and 12,300 structures, including houses, were burned. The city endured immense emotional and physical damage. Yet, many property owners in the city find themselves with little recourse for financial compensation.

In fact, over the past five years, insurance companies like State Farm, Farmers, Chubb, Liberty Mutual, and Allstate have all refused to renew policies for innumerable homeowners in the Los Angeles area, leaving residents without adequate protection for their homes. By July of 2024, State Farm alone had dropped 1,600 clients residing in the Pacific Palisades ZIP code, where damage from the fires would be some of the worst. Soaring home insurance prices have also forced lower- and middle-income residents to make the impossible decision of refusing insurance for their homes. In the wake of the most recent fires, many are not only left devastated by the destruction of their homes and the uprooting of their lives, but they are also financially stranded in the disaster’s aftermath.

All of these horrible consequences stem from a simple rule that defines much of the home insurance industry’s dealings with the public: Increased risk means increased prices. In more disaster-prone areas, the likelihood of insurance companies having to compensate homeowners is heightened by the prevalence of destructive events, and insurance companies raise premiums to remain profitable and to ensure their financial ability to cover future losses or drop clients altogether. For instance, knowing that California is highly prone to destructive wildfires, insurance companies will deny housing coverage for people in high-risk forest fire areas to avoid paying the high cost of rebuilding thousands of homes should one occur.

As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Rising insurance prices are not isolated to one region, though. Communities across the country from Kentucky to Florida to New York are now facing the brunt end of this crisis. When hurricane Ida hit New York in 2021, damages cost one woman up to $25,000 dollars out of pocket for repairs because Liberty Mutual outright rejected them coverage. This disproportionately affects low-income communities, who will face even more struggle trying to afford to pay for damages that should have been covered by their housing insurance in the first place.

Even considering the fact that the burden often falls on people purchasing insurance for their homes, increased and intensified natural disasters fundamentally have an adverse financial effect on insurance companies by making their services more expensive, which is also often accompanied by reduced coverage. Therefore, you would think that they would address the root cause of this increase in destruction—climate change.

But, many don’t. Everyday, insurance companies like Chubb, Liberty Mutual, and AIG practice hypocrisy, creating a perpetual cycle that expedites climate destruction and inequality. This is accomplished through the underwriting of fossil fuel projects, which is often cheaper for these companies because it allows them to invest and insure something deemed less “risky” that, in the short-term, will make the company more money. Insurance companies continue to underwrite pipelines for transporting fossil fuels and liquefied natural gas (LNG) infrastructure that is often built nearby vulnerable communities. The domestic insurance industry has also invested $582 billion of assets collected through client’s premiums into the fossil fuel industry. Still, climate change, caused by the emission of those exact fossil fuels into the Earth’s atmosphere, further exacerbates and increases the frequency of the (not so) natural disasters that drive up insurance prices. Essentially, these companies contribute to the climate crisis through their financial choices, and then expect frontline communities to foot the bill.

(Graphic: Green America)

The insurance industry is one of the key pillars of our society’s reliance on fossil fuels alongside the financial institutions that bankroll it and the government agencies that sign off on its expansion. When insurance companies provide coverage for fossil fuel extraction projects, they provide insurance so that in the case of a disaster like a spill or explosion, the extraction project is protected. Without insurance coverage, corporations simply cannot continue building the infrastructure that keeps us hooked on fossil fuels. For example, last year, when Chubb dropped the coverage from the Rio Grande LNG project, AIG stepped right in as an insurer on the initiative. As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Insurance companies, especially, know the risks of climate change and are vulnerable to its effects. A report by the asset manager Conning shows that 91% of insurance executives profess “significant” concern about the climate crisis. This makes efforts to persuade insurance companies on matters of climate particularly salient and realistic during these times—especially when the public wants change. According to one study, 78% of U.S. voters are at least somewhat concerned about rising property insurance costs and 67% percent are concerned about extreme weather events. Most importantly, the vast majority of the population surveyed said that insurance executives are to blame for the aforementioned rising costs and 57% said that these costs should not be passed on to customers.

Although older generations also suffer the difficulties of accessing reliable insurance and figuring out how to pick up their lives after devastating climate disasters, Gen Z is uniquely forced to come of age without the financial expectations and infrastructure that were promised to us as part of the American economic system. Affordable mortgages and insurers that will actually cover us and provide reliable and ethical insurance now seem near-impossible to access for young people, knowing the state of our climate. This has particularly impacted Gen Z because we have grown up in a time where climate disasters are stronger, more frequent, and now something of a regular occurrence. In response to these climate events becoming normal, companies will continue to increasingly deny us housing coverage and proper insurance in hopes of saving money. This calls youth across the country to take action against the hypocrisy of these companies, calling for sustainable insurance that does not fund the fossil fuel industry.

The shift to a fossil fuel-free insurance industry will not be easy, but it is now, more than ever, a necessary step toward ensuring the common good. It is, in fact, the only ethical option on behalf of corporations that are meant to protect people’s livelihoods. As youth, we demand immediate action from the individuals and corporations in power, and to those who refuse to listen to us, we have one question: Who do you expect to pay your premiums in 50 years?

The Los Angeles area began this year with some of the worst wildfires in its history. Dozens of people were killed and 200,000 were displaced. About 40,000 acres and 12,300 structures, including houses, were burned. The city endured immense emotional and physical damage. Yet, many property owners in the city find themselves with little recourse for financial compensation.

In fact, over the past five years, insurance companies like State Farm, Farmers, Chubb, Liberty Mutual, and Allstate have all refused to renew policies for innumerable homeowners in the Los Angeles area, leaving residents without adequate protection for their homes. By July of 2024, State Farm alone had dropped 1,600 clients residing in the Pacific Palisades ZIP code, where damage from the fires would be some of the worst. Soaring home insurance prices have also forced lower- and middle-income residents to make the impossible decision of refusing insurance for their homes. In the wake of the most recent fires, many are not only left devastated by the destruction of their homes and the uprooting of their lives, but they are also financially stranded in the disaster’s aftermath.

All of these horrible consequences stem from a simple rule that defines much of the home insurance industry’s dealings with the public: Increased risk means increased prices. In more disaster-prone areas, the likelihood of insurance companies having to compensate homeowners is heightened by the prevalence of destructive events, and insurance companies raise premiums to remain profitable and to ensure their financial ability to cover future losses or drop clients altogether. For instance, knowing that California is highly prone to destructive wildfires, insurance companies will deny housing coverage for people in high-risk forest fire areas to avoid paying the high cost of rebuilding thousands of homes should one occur.

As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Rising insurance prices are not isolated to one region, though. Communities across the country from Kentucky to Florida to New York are now facing the brunt end of this crisis. When hurricane Ida hit New York in 2021, damages cost one woman up to $25,000 dollars out of pocket for repairs because Liberty Mutual outright rejected them coverage. This disproportionately affects low-income communities, who will face even more struggle trying to afford to pay for damages that should have been covered by their housing insurance in the first place.

Even considering the fact that the burden often falls on people purchasing insurance for their homes, increased and intensified natural disasters fundamentally have an adverse financial effect on insurance companies by making their services more expensive, which is also often accompanied by reduced coverage. Therefore, you would think that they would address the root cause of this increase in destruction—climate change.

But, many don’t. Everyday, insurance companies like Chubb, Liberty Mutual, and AIG practice hypocrisy, creating a perpetual cycle that expedites climate destruction and inequality. This is accomplished through the underwriting of fossil fuel projects, which is often cheaper for these companies because it allows them to invest and insure something deemed less “risky” that, in the short-term, will make the company more money. Insurance companies continue to underwrite pipelines for transporting fossil fuels and liquefied natural gas (LNG) infrastructure that is often built nearby vulnerable communities. The domestic insurance industry has also invested $582 billion of assets collected through client’s premiums into the fossil fuel industry. Still, climate change, caused by the emission of those exact fossil fuels into the Earth’s atmosphere, further exacerbates and increases the frequency of the (not so) natural disasters that drive up insurance prices. Essentially, these companies contribute to the climate crisis through their financial choices, and then expect frontline communities to foot the bill.

(Graphic: Green America)

The insurance industry is one of the key pillars of our society’s reliance on fossil fuels alongside the financial institutions that bankroll it and the government agencies that sign off on its expansion. When insurance companies provide coverage for fossil fuel extraction projects, they provide insurance so that in the case of a disaster like a spill or explosion, the extraction project is protected. Without insurance coverage, corporations simply cannot continue building the infrastructure that keeps us hooked on fossil fuels. For example, last year, when Chubb dropped the coverage from the Rio Grande LNG project, AIG stepped right in as an insurer on the initiative. As climate organizers encounter a federal government unfriendly to systemic change but have made decent strides in their work with financial institutions, it is clear that targeting the private sector is imperative at this moment.

Insurance companies, especially, know the risks of climate change and are vulnerable to its effects. A report by the asset manager Conning shows that 91% of insurance executives profess “significant” concern about the climate crisis. This makes efforts to persuade insurance companies on matters of climate particularly salient and realistic during these times—especially when the public wants change. According to one study, 78% of U.S. voters are at least somewhat concerned about rising property insurance costs and 67% percent are concerned about extreme weather events. Most importantly, the vast majority of the population surveyed said that insurance executives are to blame for the aforementioned rising costs and 57% said that these costs should not be passed on to customers.

Although older generations also suffer the difficulties of accessing reliable insurance and figuring out how to pick up their lives after devastating climate disasters, Gen Z is uniquely forced to come of age without the financial expectations and infrastructure that were promised to us as part of the American economic system. Affordable mortgages and insurers that will actually cover us and provide reliable and ethical insurance now seem near-impossible to access for young people, knowing the state of our climate. This has particularly impacted Gen Z because we have grown up in a time where climate disasters are stronger, more frequent, and now something of a regular occurrence. In response to these climate events becoming normal, companies will continue to increasingly deny us housing coverage and proper insurance in hopes of saving money. This calls youth across the country to take action against the hypocrisy of these companies, calling for sustainable insurance that does not fund the fossil fuel industry.

The shift to a fossil fuel-free insurance industry will not be easy, but it is now, more than ever, a necessary step toward ensuring the common good. It is, in fact, the only ethical option on behalf of corporations that are meant to protect people’s livelihoods. As youth, we demand immediate action from the individuals and corporations in power, and to those who refuse to listen to us, we have one question: Who do you expect to pay your premiums in 50 years?