SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

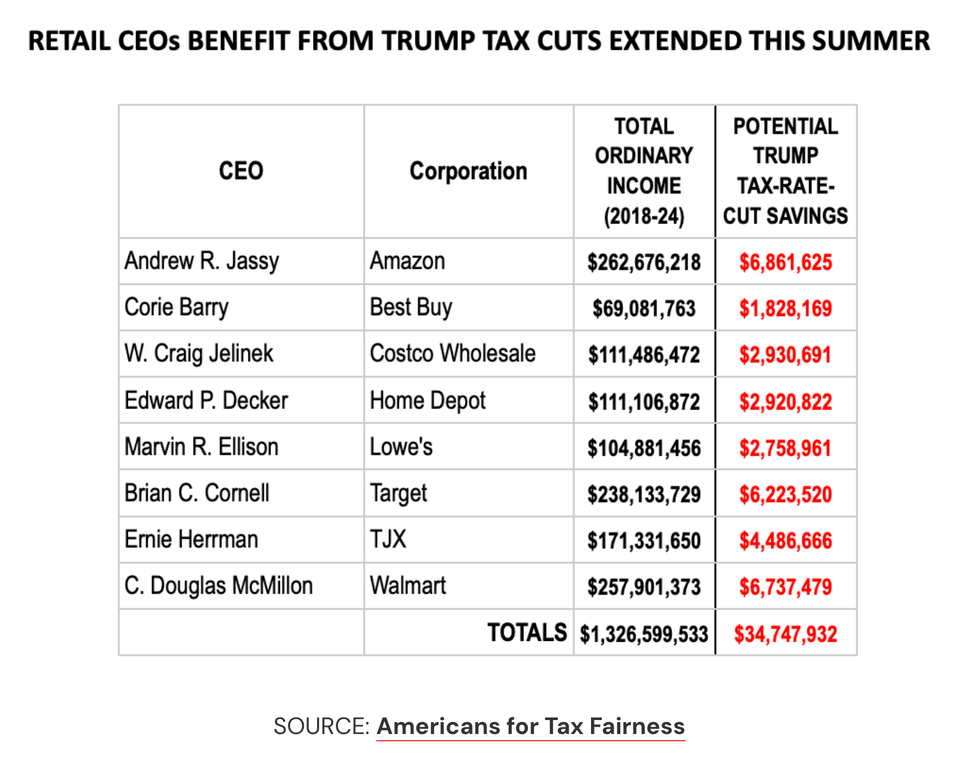

Thanks to the Trump-GOP tax law, which took effect in 2018, the companies examined in the analysis paid a tax rate of just 17.5% between 2018 and 2024—roughly half what they paid prior to the law's enactment.

"While at the same time prices have soared for consumers and retail workers remain stuck in low-wage jobs, big-store CEOs and shareholders have reaped higher profits and lower taxes," David Kass, ATF’s executive director, said in a statement. "If we want a system that alleviates economic stress on average Americans instead of exacerbating it during the holiday season, we need to raise taxes on corporations and the rich, invest in workers and families with expanded public services."

Workers at the major retailers haven't fared nearly as well. ATF noted that "the average worker at the eight stores was paid less than $32,000 in 2024."

"Amazon—the world’s largest retailer—refuses to even sit down with its employees who have formed a labor union for better pay, benefits, and working conditions," the group observed. "If Lowe’s had used the nearly $50 billion it spent on stock buybacks over the seven-year period to instead raise employee wages, its workers would have each been paid almost $200,000 more."

Across the US economy, workers are seeing wage growth stagnate amid elevated and still-rising prices, which are forcing many to skip meals and ration their medications to make ends meet.

The Labor Department said earlier this week that wage growth decelerated to 3.5% year over year—the slowest pace since before the Covid-19 pandemic. Unemployment, meanwhile, rose in November to the highest level in four years.

The ATF analysis came days after Trump delivered a lie-filled primetime speech defending his handling of the US economy as his approval ratings tanked, with American voters across party lines increasingly furious over the high costs of housing, groceries, healthcare, and other necessities.

During the speech, Trump vowed that Americans would soon "see the results of the largest tax cuts in American history."

But the richest people in the country are set to reap disproportionate benefits from the tax cuts. As Bloomberg reported earlier this week, "Many filers—particularly those who could most use the financial boost—may soon be disappointed."

"Wealthy taxpayers in high-tax states like California, New York, and New Jersey are the biggest winners," the outlet noted.

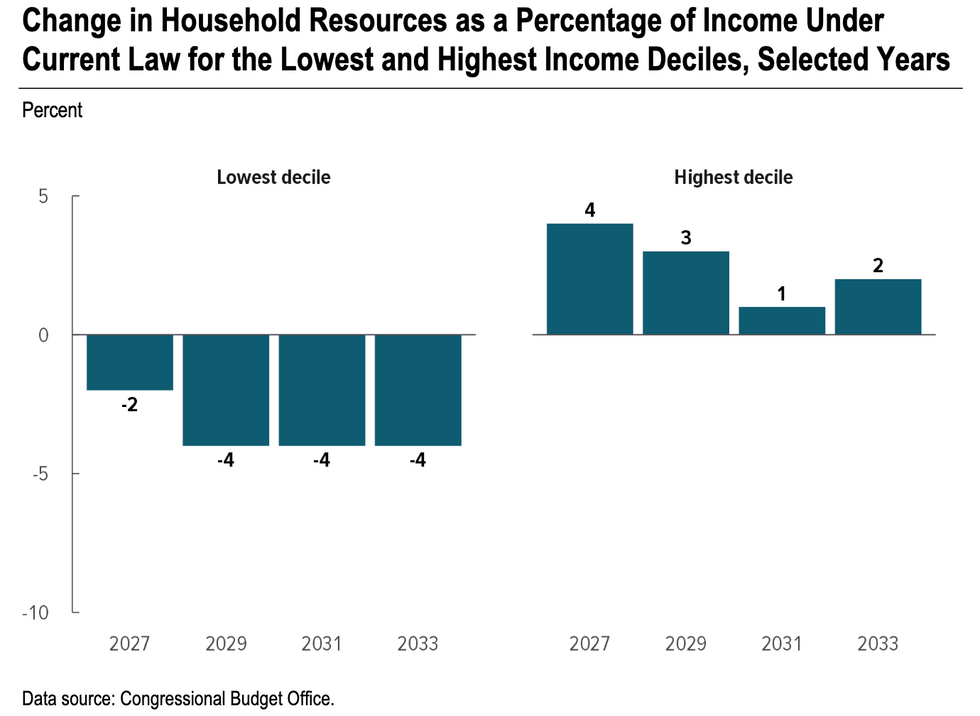

On average, according to the CBO, U.S. households would "see an increase in the resources provided to them by the government over the 2026–2034 period."

But the resources "would not be evenly distributed among households," the CBO found, estimating that "in general, resources would decrease for households in the lowest decile (tenth) of the income distribution, whereas resources would increase for households in the highest decile."

"This is what Republicans are fighting for—lining the pockets of their billionaire donors while children go hungry and families get kicked off their healthcare."

The analysis takes into account an extension of soon-to-expire provisions of the 2017 Trump-GOP tax cuts as well as Republicans' push for around $1 trillion in combined cuts to Medicaid and the Supplemental Nutrition Assistance Program (SNAP), which would primarily harm low-income Americans.

"The nonpartisan Congressional Budget Office's unprecedented analysis has confirmed what Democrats have known to be true—the GOP Tax Scam will hurt working families the most while delivering massive tax breaks for billionaires like Elon Musk," said House Minority Leader Hakeem Jeffries (D-N.Y.), who joined Rep. Brendan Boyle (D-Pa.) in requesting the distributional analysis.

"Any claims otherwise are intentionally deceptive regarding the Republican plans to rip healthcare away from nearly 14 million Americans and take food out of the mouths of millions of people, including children and seniors," said Jeffries. "Republicans are attempting to quickly jam this unpopular legislation through the House because they know that the longer they wait, the more will come to light about this cruel and unconscionable bill. For a party that claims to be for the working class, this analysis indicates the opposite."

Boyle, the ranking member of the House Budget Committee, said that "this is what Republicans are fighting for—lining the pockets of their billionaire donors while children go hungry and families get kicked off their healthcare."

"CBO's nonpartisan analysis makes it crystal clear: [President] Donald Trump and House Republicans are selling out the middle class to make the ultra-rich even richer. Every word out of Trump's mouth about helping working Americans was a lie."

The CBO also said Tuesday that the Republican reconciliation package, which Trump has championed, would trigger automatic cuts to Medicare spending—reductions that the nonpartisan body did not factor into its distributional analysis.

The CBO's analysis also did not include the impact of a tentative deal to boost the cap on state and local tax deductions (SALT), a change that would primarily benefit wealthy households.

"This reported SALT deal and accelerated Medicaid cuts would make the bill even more effective at transferring resources from low-income to high-income households," said Brendan Duke of the Center on Budget and Policy Priorities, referring to GOP hardliners' push for an earlier start date for Medicaid work requirements, which experts have decried as cruel and ineffective.

Organizers hired by Sanders in recent months "will fan out across the country this week, targeting 15 Republican-held districts" in Iowa, Wisconsin, Michigan, Arizona, and other states, the senator said.

Each of the districts was a stop on Sanders' recent "Fighting Oligarchy" tour, which drew large, energetic crowds even in areas typically seen as Republican strongholds. According to the senator's team, roughly a third of the more than 265,000 rally attendees were not registered Democrats.

The week of action kicked off with an organizing call led by Sanders, according to an announcement, with canvassing, days of action, and rallies being organized in at least eight states.

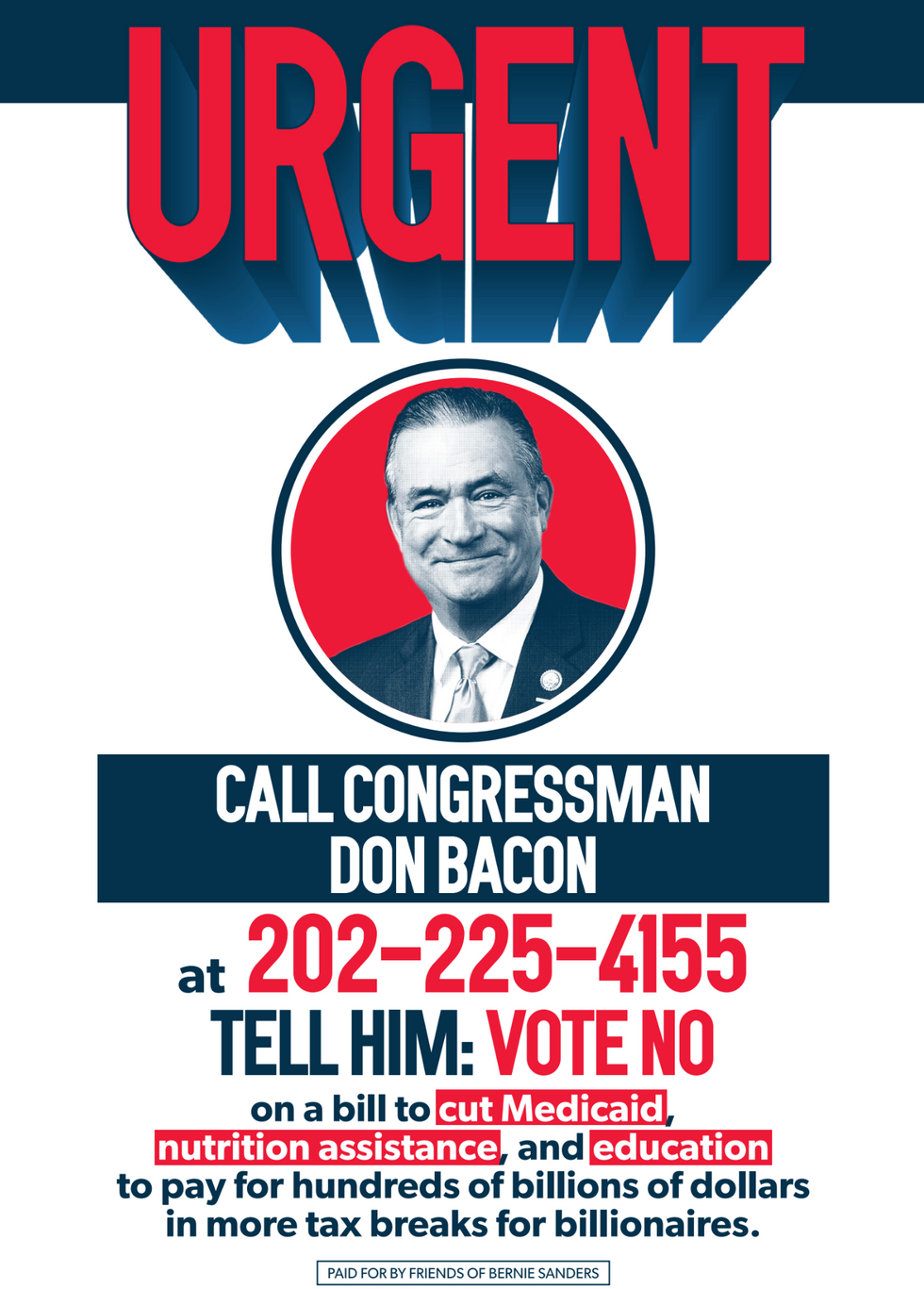

The senator's team provided a look at some of the material organizers plan to distribute during their actions. The literature urges constituents to call their representatives and urge them to vote no "on a bill to cut Medicaid, nutrition assistance, and education to pay for hundreds of billions of dollars in more tax breaks for billionaires."

One of the lawmakers targeted is Rep. Don Bacon (R-Neb.), who said last month that he would not accept more than $500 billion in Medicaid cuts over a 10-year period.

The Republican proposal includes more than $700 billion in cuts to Medicaid and would likely throw more than 8 million people off the program, according to the nonpartisan Congressional Budget Office.

Sanders said the following Republican lawmakers will also be targeted as part of the swing-district pressure campaign against the reconciliation package:

News of the actions came as Republicans on key committees prepared Tuesday for several markup hearings on their reconciliation proposals, which include around a trillion dollars in combined cuts to Medicaid and the Supplemental Nutrition Assistance Program (SNAP) as well as major tax breaks for the wealthy and large corporations.

The American Prospect's David Dayen reported last week that House Republicans deliberately scheduled the Energy and Commerce, Ways and Means, and Agriculture Committee markup hearings on the same day "to make it hard for the opposition to focus."

In a social media post on Monday, Sanders highlighted the GOP bill's proposed cuts to Medicaid and SNAP and declared, "It must be defeated."

Sanders is also working to harness the energy of his "Fighting Oligarchy" tour to recruit progressive candidates for office. Politico reported earlier this month that "the Vermont senator is teaming up with the liberal group Run for Something and other outside organizations to provide support to potential candidates."

"We want to make sure that we're not just going into these spaces and holding rallies and disappearing, and we’re not just asking people to run for office," Jeremy Slevin, a top Sanders adviser, told the outlet. "We're giving them the tools they need to actually do it."