SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

With both presidential candidates promising major reform of the federal tax system, we'll start to hear variations on the phrase, "If you want more of something, tax it less, and if you want less of something, tax it more." There's more to taxes than just raising money to support public services and determining who deserves to pay. The tax code sets some basic priorities for the economy and society, so a better way to think about taxes is to ask, "How can we improve the tax code to get the kind of economy we want?"

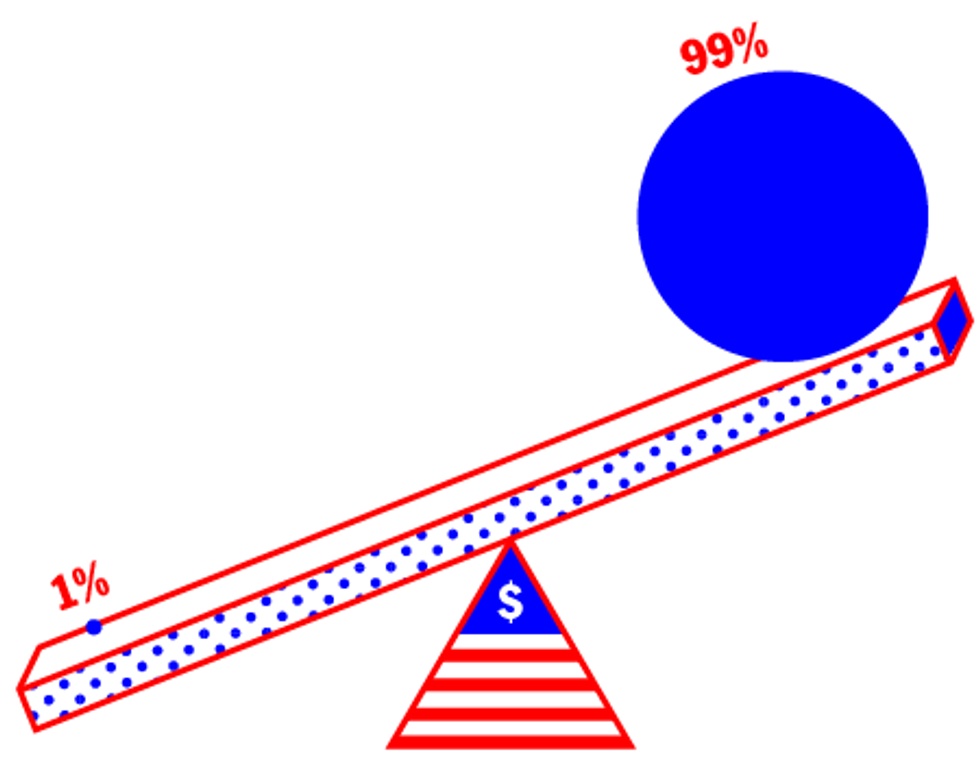

If there's one thing we should want less of in our economy, it's inequality. And what we should want more of is economic opportunity for average working Americans. While we can't and shouldn't aspire to perfect equality, the story of the last 30 years has been a staggering shift in the other direction, toward the wealthiest: The top 1 percent, who now receive almost one-fifth of all income, is the big story, but the richest 10 percent have done all right, too. Meanwhile, the income of most of the middle class began to stagnate even before the recession, and the working poor have lost ground. As soon as the recession eased, the pattern got worse, and the income of the richest one-10th of 1 percent increased by more than 20 percent in 2010 alone.

We could use taxes and social programs to redress inequality directly, raising taxes on the wealthiest and using the revenues--after we reduce the deficit and shore up Medicare--to build support for the middle class and the poor. The economists Thomas Piketty and Emanuel Saez, the preeminent experts on inequality, have demonstrated that the top tax rate could go as high as 83 percent without harming economic growth. And in fact, our top rates have been even higher than that at times of rapid growth. But in a world where the very wealthiest hold enormous political power, this is at best a theoretical argument. High nominal tax rates like those of the prosperous 1950s are far outside the scope of political possibility.

But if we think of the tax code as a set of incentives, rather than simply a mechanism to redistribute income, there are creative and effective ways to moderate the extremes of wealth, boost the pay of ordinary workers, make American companies more stable and efficient, and reduce the long-term federal budget deficit.

Start by looking at who the top 1 percent really are; Sure, some of them are athletes, musicians, and movie stars able to command huge rewards in open auctions for their talents, but according to an analysis of tax return data by Jon Bakija and two colleagues at Williams College, people who make their living in arts, media, or sports comprise only 1.6 percent of the top 1 percent. Financial professionals, such as hedge fund managers, make up 13 percent. Most people in the 1 percent are simply executives at non-financial businesses--CEOs, CFOs, COOs, vice presidents, and whatever other inflated titles they've conjured up. Corporate executives make up 31 percent of the top 1 percent, and at the highest tier, among the top .01 percent, corporate executives from non-financial companies make up 40 percent of the total.

An astonishing contributor to inequality, then, is corporate bosses taking a larger share of the company's revenue for themselves. In 2008, the average CEO earned 300 times the pay of the average worker. That's way out of line by historic standards: In 1980, the ratio was just 40 to 1. And it's way out of line by international standards--only in the United Kingdom is executive pay comparable; in Japan, executive compensation relative to the pay of average workers is one-fifth of what it is in the United States. It's also out of line at companies that demonstrate that you don't need to pay the CEO like a king in order to excel: At Whole Foods Markets, the CEO's compensation is capped at 14 times the average employee salary.

Because current CEO pay numbers are so far out of the ordinary, it's hard to argue that they are a natural outcome of the market. In fact, the tax code, with its low taxes on individuals and preference for capital gains, already has a lot to do with why companies overpay CEOs. In 1993, Congress passed a law intended to moderate CEO pay, which limited the tax deductibility of executive salaries over $1 million. But the law specifically exempted "performance-based" pay, like payment in stock options or grants of restricted stock. The response showed that companies do adjust their behavior in response to tax incentives, but it did not reduce CEO pay: CEOs simply chose to take their pay in the form of stock options.

But stock options don't create an incentive to help the company do better. They create an incentive to manipulate earnings in order to push up the stock price in the short term, and to focus on finance rather than on what the company makes. With the possibility of becoming extraordinarily wealthy in just a few years, executives like HP's Carly Fiorina made short-sighted decisions that actually weakened their companies.

Executive pay declined a bit during the recession, but in 2010 the pay package for the CEO of an S&P 500 company averaged $9 million, up 24 percent from a year earlier and higher than in 2007, when the economy and stock market were booming. As CNBC put it, "In the boardroom, it's as if the Great Recession never happened."

For most workers, though, the recession not only happened, it's continuing. When CEOs push up their own salaries while laying off workers, closing divisions, and keeping wages down, it represents a specific decision to increase inequality, raising incomes at the top and lowering them in the middle.

The tax code created the incentives for these decisions, and the tax code can be part of the solution. The first step is to end the preferential treatment of income from capital gains, which economists like Princeton's Alan Blinder have shown to have no lasting effect on total investment or the economy. But we can and should go further, actively using the corporate tax code to create a real incentive to pay CEOs less, and workers more, by linking the head honcho's compensation to both employee salaries and tax rates.

Here's how the idea could work. The current corporate tax rate is a flat 35 percent. In an equity-based corporate tax system, companies with a pay ratio at the historic norm of 40:1, or even up to 60:1, would pay the existing rate and be able to deduct executive pay. But companies that pay their top executives more than 60 times the average worker (including employees in overseas subsidiaries) would pay a higher rate, 40 percent, and those with extreme pay differentials, 80:1 or higher, would pay 45 percent.

Companies with more equitable pay structures, including Whole Foods, would get a tax break, paying as little as 25 percent. This tax structure gives companies far more flexibility than a flat ceiling on executive pay. C-Suite executives could still pay themselves whatever they wanted, but they would have to explain to their boards why it was worth paying a higher tax rate as a result. Maybe their boards will decide that they are so brilliant that it's worth it.

Most companies will start off far above the historic average, so this new corporate tax structure is likely to raise significant revenue. But it's hard to say how much, because corporations will have three choices: They can pay the higher tax rates, bring executive pay under control, or raise the pay of average workers. It's difficult to estimate what combination of approaches will prevail, but whatever happens, it will be bring broad benefits to society as a whole, far outweighing the impact on the federal budget.

If the equity-based corporate tax code encourages companies to share more of the gains from productivity with workers, it will not only increase fairness, but by putting more money in the hands of middle-income families, it will boost consumer demand--and thus the entire economy. If it causes companies to reduce CEO pay, it might encourage CEOs to think more about the long-term good of the company and less about how to get personally rich. And studies show that workers are often discouraged and less productive when they feel the overall pay structure is unfair, so reduced executive pay might improve efficiency as well.

With both presidential candidates promising major reform of the federal tax system, we'll start to hear variations on the phrase, "If you want more of something, tax it less, and if you want less of something, tax it more." There's more to taxes than just raising money to support public services and determining who deserves to pay. The tax code sets some basic priorities for the economy and society, so a better way to think about taxes is to ask, "How can we improve the tax code to get the kind of economy we want?"

If there's one thing we should want less of in our economy, it's inequality. And what we should want more of is economic opportunity for average working Americans. While we can't and shouldn't aspire to perfect equality, the story of the last 30 years has been a staggering shift in the other direction, toward the wealthiest: The top 1 percent, who now receive almost one-fifth of all income, is the big story, but the richest 10 percent have done all right, too. Meanwhile, the income of most of the middle class began to stagnate even before the recession, and the working poor have lost ground. As soon as the recession eased, the pattern got worse, and the income of the richest one-10th of 1 percent increased by more than 20 percent in 2010 alone.

We could use taxes and social programs to redress inequality directly, raising taxes on the wealthiest and using the revenues--after we reduce the deficit and shore up Medicare--to build support for the middle class and the poor. The economists Thomas Piketty and Emanuel Saez, the preeminent experts on inequality, have demonstrated that the top tax rate could go as high as 83 percent without harming economic growth. And in fact, our top rates have been even higher than that at times of rapid growth. But in a world where the very wealthiest hold enormous political power, this is at best a theoretical argument. High nominal tax rates like those of the prosperous 1950s are far outside the scope of political possibility.

But if we think of the tax code as a set of incentives, rather than simply a mechanism to redistribute income, there are creative and effective ways to moderate the extremes of wealth, boost the pay of ordinary workers, make American companies more stable and efficient, and reduce the long-term federal budget deficit.

Start by looking at who the top 1 percent really are; Sure, some of them are athletes, musicians, and movie stars able to command huge rewards in open auctions for their talents, but according to an analysis of tax return data by Jon Bakija and two colleagues at Williams College, people who make their living in arts, media, or sports comprise only 1.6 percent of the top 1 percent. Financial professionals, such as hedge fund managers, make up 13 percent. Most people in the 1 percent are simply executives at non-financial businesses--CEOs, CFOs, COOs, vice presidents, and whatever other inflated titles they've conjured up. Corporate executives make up 31 percent of the top 1 percent, and at the highest tier, among the top .01 percent, corporate executives from non-financial companies make up 40 percent of the total.

An astonishing contributor to inequality, then, is corporate bosses taking a larger share of the company's revenue for themselves. In 2008, the average CEO earned 300 times the pay of the average worker. That's way out of line by historic standards: In 1980, the ratio was just 40 to 1. And it's way out of line by international standards--only in the United Kingdom is executive pay comparable; in Japan, executive compensation relative to the pay of average workers is one-fifth of what it is in the United States. It's also out of line at companies that demonstrate that you don't need to pay the CEO like a king in order to excel: At Whole Foods Markets, the CEO's compensation is capped at 14 times the average employee salary.

Because current CEO pay numbers are so far out of the ordinary, it's hard to argue that they are a natural outcome of the market. In fact, the tax code, with its low taxes on individuals and preference for capital gains, already has a lot to do with why companies overpay CEOs. In 1993, Congress passed a law intended to moderate CEO pay, which limited the tax deductibility of executive salaries over $1 million. But the law specifically exempted "performance-based" pay, like payment in stock options or grants of restricted stock. The response showed that companies do adjust their behavior in response to tax incentives, but it did not reduce CEO pay: CEOs simply chose to take their pay in the form of stock options.

But stock options don't create an incentive to help the company do better. They create an incentive to manipulate earnings in order to push up the stock price in the short term, and to focus on finance rather than on what the company makes. With the possibility of becoming extraordinarily wealthy in just a few years, executives like HP's Carly Fiorina made short-sighted decisions that actually weakened their companies.

Executive pay declined a bit during the recession, but in 2010 the pay package for the CEO of an S&P 500 company averaged $9 million, up 24 percent from a year earlier and higher than in 2007, when the economy and stock market were booming. As CNBC put it, "In the boardroom, it's as if the Great Recession never happened."

For most workers, though, the recession not only happened, it's continuing. When CEOs push up their own salaries while laying off workers, closing divisions, and keeping wages down, it represents a specific decision to increase inequality, raising incomes at the top and lowering them in the middle.

The tax code created the incentives for these decisions, and the tax code can be part of the solution. The first step is to end the preferential treatment of income from capital gains, which economists like Princeton's Alan Blinder have shown to have no lasting effect on total investment or the economy. But we can and should go further, actively using the corporate tax code to create a real incentive to pay CEOs less, and workers more, by linking the head honcho's compensation to both employee salaries and tax rates.

Here's how the idea could work. The current corporate tax rate is a flat 35 percent. In an equity-based corporate tax system, companies with a pay ratio at the historic norm of 40:1, or even up to 60:1, would pay the existing rate and be able to deduct executive pay. But companies that pay their top executives more than 60 times the average worker (including employees in overseas subsidiaries) would pay a higher rate, 40 percent, and those with extreme pay differentials, 80:1 or higher, would pay 45 percent.

Companies with more equitable pay structures, including Whole Foods, would get a tax break, paying as little as 25 percent. This tax structure gives companies far more flexibility than a flat ceiling on executive pay. C-Suite executives could still pay themselves whatever they wanted, but they would have to explain to their boards why it was worth paying a higher tax rate as a result. Maybe their boards will decide that they are so brilliant that it's worth it.

Most companies will start off far above the historic average, so this new corporate tax structure is likely to raise significant revenue. But it's hard to say how much, because corporations will have three choices: They can pay the higher tax rates, bring executive pay under control, or raise the pay of average workers. It's difficult to estimate what combination of approaches will prevail, but whatever happens, it will be bring broad benefits to society as a whole, far outweighing the impact on the federal budget.

If the equity-based corporate tax code encourages companies to share more of the gains from productivity with workers, it will not only increase fairness, but by putting more money in the hands of middle-income families, it will boost consumer demand--and thus the entire economy. If it causes companies to reduce CEO pay, it might encourage CEOs to think more about the long-term good of the company and less about how to get personally rich. And studies show that workers are often discouraged and less productive when they feel the overall pay structure is unfair, so reduced executive pay might improve efficiency as well.

With both presidential candidates promising major reform of the federal tax system, we'll start to hear variations on the phrase, "If you want more of something, tax it less, and if you want less of something, tax it more." There's more to taxes than just raising money to support public services and determining who deserves to pay. The tax code sets some basic priorities for the economy and society, so a better way to think about taxes is to ask, "How can we improve the tax code to get the kind of economy we want?"

If there's one thing we should want less of in our economy, it's inequality. And what we should want more of is economic opportunity for average working Americans. While we can't and shouldn't aspire to perfect equality, the story of the last 30 years has been a staggering shift in the other direction, toward the wealthiest: The top 1 percent, who now receive almost one-fifth of all income, is the big story, but the richest 10 percent have done all right, too. Meanwhile, the income of most of the middle class began to stagnate even before the recession, and the working poor have lost ground. As soon as the recession eased, the pattern got worse, and the income of the richest one-10th of 1 percent increased by more than 20 percent in 2010 alone.

We could use taxes and social programs to redress inequality directly, raising taxes on the wealthiest and using the revenues--after we reduce the deficit and shore up Medicare--to build support for the middle class and the poor. The economists Thomas Piketty and Emanuel Saez, the preeminent experts on inequality, have demonstrated that the top tax rate could go as high as 83 percent without harming economic growth. And in fact, our top rates have been even higher than that at times of rapid growth. But in a world where the very wealthiest hold enormous political power, this is at best a theoretical argument. High nominal tax rates like those of the prosperous 1950s are far outside the scope of political possibility.

But if we think of the tax code as a set of incentives, rather than simply a mechanism to redistribute income, there are creative and effective ways to moderate the extremes of wealth, boost the pay of ordinary workers, make American companies more stable and efficient, and reduce the long-term federal budget deficit.

Start by looking at who the top 1 percent really are; Sure, some of them are athletes, musicians, and movie stars able to command huge rewards in open auctions for their talents, but according to an analysis of tax return data by Jon Bakija and two colleagues at Williams College, people who make their living in arts, media, or sports comprise only 1.6 percent of the top 1 percent. Financial professionals, such as hedge fund managers, make up 13 percent. Most people in the 1 percent are simply executives at non-financial businesses--CEOs, CFOs, COOs, vice presidents, and whatever other inflated titles they've conjured up. Corporate executives make up 31 percent of the top 1 percent, and at the highest tier, among the top .01 percent, corporate executives from non-financial companies make up 40 percent of the total.

An astonishing contributor to inequality, then, is corporate bosses taking a larger share of the company's revenue for themselves. In 2008, the average CEO earned 300 times the pay of the average worker. That's way out of line by historic standards: In 1980, the ratio was just 40 to 1. And it's way out of line by international standards--only in the United Kingdom is executive pay comparable; in Japan, executive compensation relative to the pay of average workers is one-fifth of what it is in the United States. It's also out of line at companies that demonstrate that you don't need to pay the CEO like a king in order to excel: At Whole Foods Markets, the CEO's compensation is capped at 14 times the average employee salary.

Because current CEO pay numbers are so far out of the ordinary, it's hard to argue that they are a natural outcome of the market. In fact, the tax code, with its low taxes on individuals and preference for capital gains, already has a lot to do with why companies overpay CEOs. In 1993, Congress passed a law intended to moderate CEO pay, which limited the tax deductibility of executive salaries over $1 million. But the law specifically exempted "performance-based" pay, like payment in stock options or grants of restricted stock. The response showed that companies do adjust their behavior in response to tax incentives, but it did not reduce CEO pay: CEOs simply chose to take their pay in the form of stock options.

But stock options don't create an incentive to help the company do better. They create an incentive to manipulate earnings in order to push up the stock price in the short term, and to focus on finance rather than on what the company makes. With the possibility of becoming extraordinarily wealthy in just a few years, executives like HP's Carly Fiorina made short-sighted decisions that actually weakened their companies.

Executive pay declined a bit during the recession, but in 2010 the pay package for the CEO of an S&P 500 company averaged $9 million, up 24 percent from a year earlier and higher than in 2007, when the economy and stock market were booming. As CNBC put it, "In the boardroom, it's as if the Great Recession never happened."

For most workers, though, the recession not only happened, it's continuing. When CEOs push up their own salaries while laying off workers, closing divisions, and keeping wages down, it represents a specific decision to increase inequality, raising incomes at the top and lowering them in the middle.

The tax code created the incentives for these decisions, and the tax code can be part of the solution. The first step is to end the preferential treatment of income from capital gains, which economists like Princeton's Alan Blinder have shown to have no lasting effect on total investment or the economy. But we can and should go further, actively using the corporate tax code to create a real incentive to pay CEOs less, and workers more, by linking the head honcho's compensation to both employee salaries and tax rates.

Here's how the idea could work. The current corporate tax rate is a flat 35 percent. In an equity-based corporate tax system, companies with a pay ratio at the historic norm of 40:1, or even up to 60:1, would pay the existing rate and be able to deduct executive pay. But companies that pay their top executives more than 60 times the average worker (including employees in overseas subsidiaries) would pay a higher rate, 40 percent, and those with extreme pay differentials, 80:1 or higher, would pay 45 percent.

Companies with more equitable pay structures, including Whole Foods, would get a tax break, paying as little as 25 percent. This tax structure gives companies far more flexibility than a flat ceiling on executive pay. C-Suite executives could still pay themselves whatever they wanted, but they would have to explain to their boards why it was worth paying a higher tax rate as a result. Maybe their boards will decide that they are so brilliant that it's worth it.

Most companies will start off far above the historic average, so this new corporate tax structure is likely to raise significant revenue. But it's hard to say how much, because corporations will have three choices: They can pay the higher tax rates, bring executive pay under control, or raise the pay of average workers. It's difficult to estimate what combination of approaches will prevail, but whatever happens, it will be bring broad benefits to society as a whole, far outweighing the impact on the federal budget.

If the equity-based corporate tax code encourages companies to share more of the gains from productivity with workers, it will not only increase fairness, but by putting more money in the hands of middle-income families, it will boost consumer demand--and thus the entire economy. If it causes companies to reduce CEO pay, it might encourage CEOs to think more about the long-term good of the company and less about how to get personally rich. And studies show that workers are often discouraged and less productive when they feel the overall pay structure is unfair, so reduced executive pay might improve efficiency as well.