SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

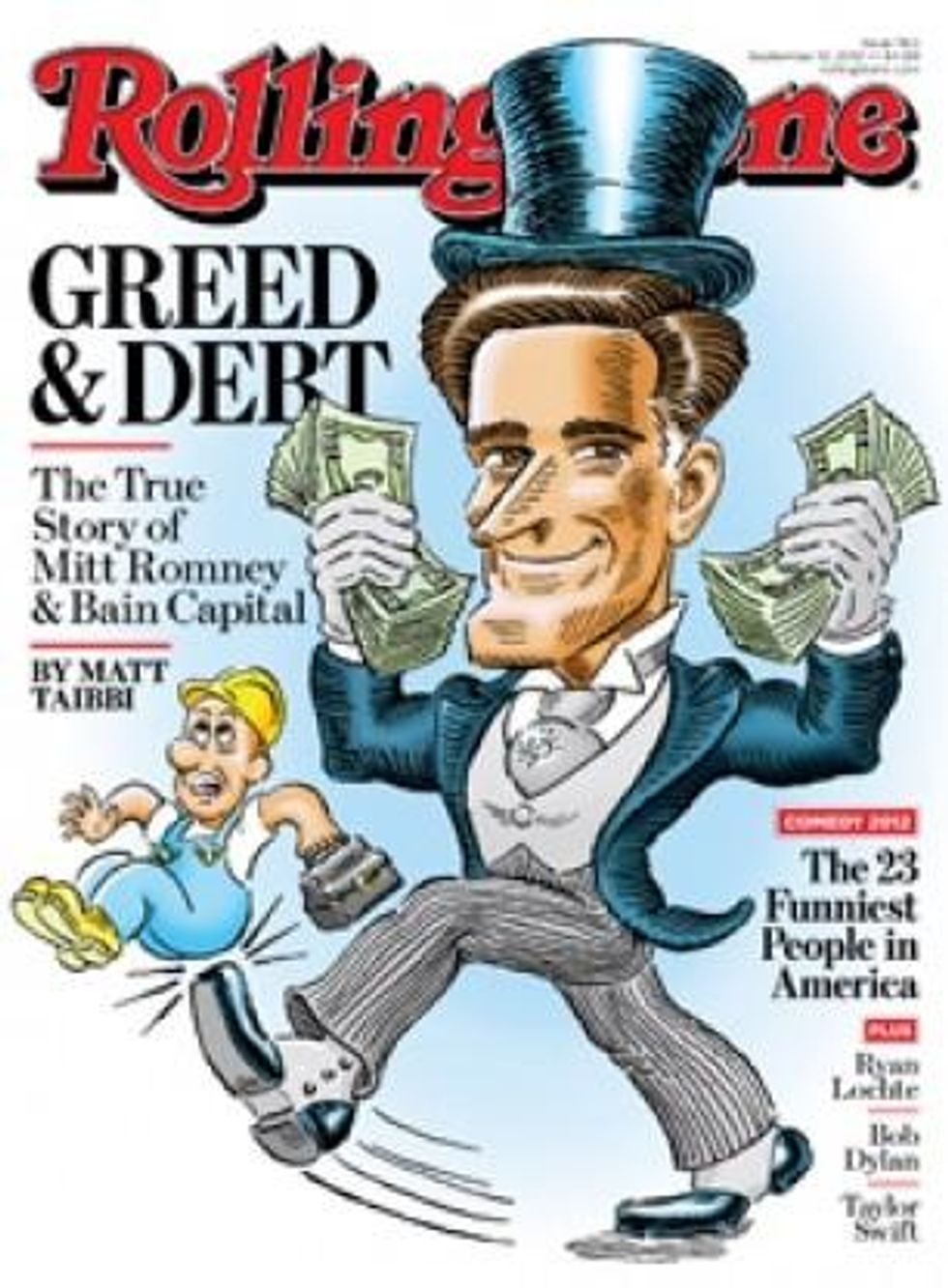

The great criticism of Mitt Romney, from both sides of the aisle, has always been that he doesn't stand for anything. He's a flip-flopper, they say, a lightweight, a cardboard opportunist who'll say anything to get elected.

The critics couldn't be more wrong. Mitt Romney is no tissue-paper man. He's closer to being a revolutionary, a backward-world version of Che or Trotsky, with tweezed nostrils instead of a beard, a half-Windsor instead of a leather jerkin. His legendary flip-flops aren't the lies of a bumbling opportunist - they're the confident prevarications of a man untroubled by misleading the nonbeliever in pursuit of a single, all-consuming goal. Romney has a vision, and he's trying for something big: We've just been too slow to sort out what it is, just as we've been slow to grasp the roots of the radical economic changes that have swept the country in the last generation.

The incredible untold story of the 2012 election so far is that Romney's run has been a shimmering pearl of perfect political hypocrisy, which he's somehow managed to keep hidden, even with thousands of cameras following his every move. And the drama of this rhetorical high-wire act was ratcheted up even further when Romney chose his running mate, Rep. Paul Ryan of Wisconsin - like himself, a self-righteously anal, thin-lipped, Whitest Kids U Know penny pincher who'd be honored to tell Oliver Twist there's no more soup left. By selecting Ryan, Romney, the hard-charging, chameleonic champion of a disgraced-yet-defiant Wall Street, officially succeeded in moving the battle lines in the 2012 presidential race.

Like John McCain four years before, Romney desperately needed a vice-presidential pick that would change the game. But where McCain bet on a combustive mix of clueless novelty and suburban sexual tension named Sarah Palin, Romney bet on an idea. He said as much when he unveiled his choice of Ryan, the author of a hair-raising budget-cutting plan best known for its willingness to slash the sacred cows of Medicare and Medicaid. "Paul Ryan has become an intellectual leader of the Republican Party," Romney told frenzied Republican supporters in Norfolk, Virginia, standing before the reliably jingoistic backdrop of a floating warship. "He understands the fiscal challenges facing America: our exploding deficits and crushing debt."

Debt, debt, debt. If the Republican Party had a James Carville, this is what he would have said to win Mitt over, in whatever late-night war room session led to the Ryan pick: "It's the debt, stupid." This is the way to defeat Barack Obama: to recast the race as a jeremiad against debt, something just about everybody who's ever gotten a bill in the mail hates on a primal level.

Last May, in a much-touted speech in Iowa, Romney used language that was literally inflammatory to describe America's federal borrowing. "A prairie fire of debt is sweeping across Iowa and our nation," he declared. "Every day we fail to act, that fire gets closer to the homes and children we love." Our collective debt is no ordinary problem: According to Mitt, it's going to burn our children alive.

And this is where we get to the hypocrisy at the heart of Mitt Romney. Everyone knows that he is fantastically rich, having scored great success, the legend goes, as a "turnaround specialist," a shrewd financial operator who revived moribund companies as a high-priced consultant for a storied Wall Street private equity firm. But what most voters don't know is the way Mitt Romney actually made his fortune: by borrowing vast sums of money that other people were forced to pay back. This is the plain, stark reality that has somehow eluded America's top political journalists for two consecutive presidential campaigns: Mitt Romney is one of the greatest and most irresponsible debt creators of all time. In the past few decades, in fact, Romney has piled more debt onto more unsuspecting companies, written more gigantic checks that other people have to cover, than perhaps all but a handful of people on planet Earth.

By making debt the centerpiece of his campaign, Romney was making a calculated bluff of historic dimensions - placing a massive all-in bet on the rank incompetence of the American press corps. The result has been a brilliant comedy: A man makes a $250 million fortune loading up companies with debt and then extracting million-dollar fees from those same companies, in exchange for the generous service of telling them who needs to be fired in order to finance the debt payments he saddled them with in the first place. That same man then runs for president riding an image of children roasting on flames of debt, choosing as his running mate perhaps the only politician in America more pompous and self-righteous on the subject of the evils of borrowed money than the candidate himself. If Romney pulls off this whopper, you'll have to tip your hat to him: No one in history has ever successfully run for president riding this big of a lie. It's almost enough to make you think he really is qualified for the White House.

The unlikeliness of Romney's gambit isn't simply a reflection of his own artlessly unapologetic mindset - it stands as an emblem for the resiliency of the entire sociopathic Wall Street set he represents. Four years ago, the Mitt Romneys of the world nearly destroyed the global economy with their greed, shortsightedness and - most notably - wildly irresponsible use of debt in pursuit of personal profit. The sight was so disgusting that people everywhere were ready to drop an H-bomb on Lower Manhattan and bayonet the survivors. But today that same insane greed ethos, that same belief in the lunatic pursuit of instant borrowed millions - it's dusted itself off, it's had a shave and a shoeshine, and it's back out there running for president.

Mitt Romney, it turns out, is the perfect frontman for Wall Street's greed revolution. He's not a two-bit, shifty-eyed huckster like Lloyd Blankfein. He's not a sighing, eye-rolling, arrogant jerkwad like Jamie Dimon. But Mitt believes the same things those guys believe: He's been right with them on the front lines of the financialization revolution, a decades-long campaign in which the old, simple, let's-make-stuff-and-sell-it manufacturing economy was replaced with a new, highly complex, let's-take-stuff-and-trash-it financial economy. Instead of cars and airplanes, we built swaps, CDOs and other toxic financial products. Instead of building new companies from the ground up, we took out massive bank loans and used them to acquire existing firms, liquidating every asset in sight and leaving the target companies holding the note. The new borrow-and-conquer economy was morally sanctified by an almost religious faith in the grossly euphemistic concept of "creative destruction," and amounted to a total abdication of collective responsibility by America's rich, whose new thing was making assloads of money in ever-shorter campaigns of economic conquest, sending the proceeds offshore, and shrugging as the great towns and factories their parents and grandparents built were shuttered and boarded up, crushed by a true prairie fire of debt.

Mitt Romney - a man whose own father built cars and nurtured communities, and was one of the old-school industrial anachronisms pushed aside by the new generation's wealth grab - has emerged now to sell this make-nothing, take-everything, screw-everyone ethos to the world. He's Gordon Gekko, but a new and improved version, with better PR - and a bigger goal. A takeover artist all his life, Romney is now trying to take over America itself. And if his own history is any guide, we'll all end up paying for the acquisition.

Willard "Mitt" Romney's background in many ways suggests a man who was born to be president - disgustingly rich from birth, raised in prep schools, no early exposure to minorities outside of maids, a powerful daddy to clean up his missteps, and timely exemptions from military service. In Romney's bio there are some eerie early-life similarities to other recent presidential figures. (Is America really ready for another Republican president who was a prep-school cheerleader?) And like other great presidential double-talkers such as Bill Clinton and George W. Bush, Romney has shown particular aptitude in the area of telling multiple factual versions of his own life story.

"I longed in many respects to actually be in Vietnam and be representing our country there," he claimed years after the war. To a different audience, he said, "I was not planning on signing up for the military. It was not my desire to go off and serve in Vietnam."

Like John F. Kennedy and George W. Bush, men whose way into power was smoothed by celebrity fathers but who rebelled against their parental legacy as mature politicians, Mitt Romney's career has been both a tribute to and a repudiation of his famous father. George Romney in the 1950s became CEO of American Motors Corp., made a modest fortune betting on energy efficiency in an age of gas guzzlers and ended up serving as governor of the state of Michigan only two generations removed from the Romney clan's tradition of polygamy. For Mitt, who grew up worshipping his tall, craggily handsome, politically moderate father, life was less rocky: Cranbrook prep school in suburban Detroit, followed by Stanford in the Sixties, a missionary term in which he spent two and a half years trying (as he said) to persuade the French to "give up your wine," and Harvard Business School in the Seventies. Then, faced with making a career choice, Mitt chose an odd one: Already married and a father of two, he left Harvard and eschewed both politics and the law to enter the at-the-time unsexy world of financial consulting.

"When you get out of a place like Harvard, you can do anything - at least in the old days you could," says a prominent corporate lawyer on Wall Street who is familiar with Romney's career. "But he comes out, he not only has a Harvard Business School degree, he's got a national pedigree with his name. He could have done anything - but what does he do? He says, 'I'm going to spend my life loading up distressed companies with debt.' "

Romney started off at the Boston Consulting Group, where he showed an aptitude for crunching numbers and glad-handing clients. Then, in 1977, he joined a young entrepreneur named Bill Bain at a firm called Bain & Company, where he worked for six years before being handed the reins of a new firm-within-a-firm called Bain Capital.

In Romney's version of the tale, Bain Capital - which evolved into what is today known as a private equity firm - specialized in turning around moribund companies (Romney even wrote a book called Turnaround that complements his other nauseatingly self-complimentary book, No Apology) and helped create the Staples office-supply chain. On the campaign trail, Romney relentlessly trades on his own self-perpetuated reputation as a kind of altruistic rescuer of failing enterprises, never missing an opportunity to use the word "help" or "helped" in his description of what he and Bain did for companies. He might, for instance, describe himself as having been "deeply involved in helping other businesses" or say he "helped create tens of thousands of jobs."

The reality is that toward the middle of his career at Bain, Romney made a fateful strategic decision: He moved away from creating companies like Staples through venture capital schemes, and toward a business model that involved borrowing huge sums of money to take over existing firms, then extracting value from them by force. He decided, as he later put it, that "there's a lot greater risk in a startup than there is in acquiring an existing company." In the Eighties, when Romney made this move, this form of financial piracy became known as a leveraged buyout, and it achieved iconic status thanks to Gordon Gekko in Wall Street. Gekko's business strategy was essentially identical to the Romney-Bain model, only Gekko called himself a "liberator" of companies instead of a "helper."

Here's how Romney would go about "liberating" a company: A private equity firm like Bain typically seeks out floundering businesses with good cash flows. It then puts down a relatively small amount of its own money and runs to a big bank like Goldman Sachs or Citigroup for the rest of the financing. (Most leveraged buyouts are financed with 60 to 90 percent borrowed cash.) The takeover firm then uses that borrowed money to buy a controlling stake in the target company, either with or without its consent. When an LBO is done without the consent of the target, it's called a hostile takeover; such thrilling acts of corporate piracy were made legend in the Eighties, most notably the 1988 attack by notorious corporate raiders Kohlberg Kravis Roberts against RJR Nabisco, a deal memorialized in the book Barbarians at the Gate.

Romney and Bain avoided the hostile approach, preferring to secure the cooperation of their takeover targets by buying off a company's management with lucrative bonuses. Once management is on board, the rest is just math. So if the target company is worth $500 million, Bain might put down $20 million of its own cash, then borrow $350 million from an investment bank to take over a controlling stake.

But here's the catch. When Bain borrows all of that money from the bank, it's the target company that ends up on the hook for all of the debt.

Now your troubled firm - let's say you make tricycles in Alabama - has been taken over by a bunch of slick Wall Street dudes who kicked in as little as five percent as a down payment. So in addition to whatever problems you had before, Tricycle Inc. now owes Goldman or Citigroup $350 million. With all that new debt service to pay, the company's bottom line is suddenly untenable: You almost have to start firing people immediately just to get your costs down to a manageable level.

"That interest," says Lynn Turner, former chief accountant of the Securities and Exchange Commission, "just sucks the profit out of the company."

Fortunately, the geniuses at Bain who now run the place are there to help tell you whom to fire. And for the service it performs cutting your company's costs to help you pay off the massive debt that it, Bain, saddled your company with in the first place, Bain naturally charges a management fee, typically millions of dollars a year. So Tricycle Inc. now has two gigantic new burdens it never had before Bain Capital stepped into the picture: tens of millions in annual debt service, and millions more in "management fees." Since the initial acquisition of Tricycle Inc. was probably greased by promising the company's upper management lucrative bonuses, all that pain inevitably comes out of just one place: the benefits and payroll of the hourly workforce.

Once all that debt is added, one of two things can happen. The company can fire workers and slash benefits to pay off all its new obligations to Goldman Sachs and Bain, leaving it ripe to be resold by Bain at a huge profit. Or it can go bankrupt - this happens after about seven percent of all private equity buyouts - leaving behind one or more shuttered factory towns. Either way, Bain wins. By power-sucking cash value from even the most rapidly dying firms, private equity raiders like Bain almost always get their cash out before a target goes belly up.

This business model wasn't really "helping," of course - and it wasn't new. Fans of mob movies will recognize what's known as the "bust-out," in which a gangster takes over a restaurant or sporting goods store and then monetizes his investment by running up giant debts on the company's credit line. (Think Paulie buying all those cases of Cutty Sark in Goodfellas.) When the note comes due, the mobster simply torches the restaurant and collects the insurance money. Reduced to their most basic level, the leveraged buyouts engineered by Romney followed exactly the same business model. "It's the bust-out," one Wall Street trader says with a laugh. "That's all it is."

Private equity firms aren't necessarily evil by definition. There are many stories of successful turnarounds fueled by private equity, often involving multiple floundering businesses that are rolled into a single entity, eliminating duplicative overhead. Experian, the giant credit-rating tyrant, was acquired by Bain in the Nineties and went on to become an industry leader.

But there's a key difference between private equity firms and the businesses that were America's original industrial cornerstones, like the elder Romney's AMC. Everyone had a stake in the success of those old businesses, which spread prosperity by putting people to work. But even private equity's most enthusiastic adherents have difficulty explaining its benefit to society. Marc Wolpow, a former Bain colleague of Romney's, told reporters during Mitt's first Senate run that Romney erred in trying to sell his business as good for everyone. "I believed he was making a mistake by framing himself as a job creator," said Wolpow. "That was not his or Bain's or the industry's primary objective. The objective of the LBO business is maximizing returns for investors." When it comes to private equity, American workers - not to mention their families and communities - simply don't enter into the equation.

Take a typical Bain transaction involving an Indiana-based company called American Pad and Paper. Bain bought Ampad in 1992 for just $5 million, financing the rest of the deal with borrowed cash. Within three years, Ampad was paying $60 million in annual debt payments, plus an additional $7 million in management fees. A year later, Bain led Ampad to go public, cashed out about $50 million in stock for itself and its investors, charged the firm $2 million for arranging the IPO and pocketed another $5 million in "management" fees. Ampad wound up going bankrupt, and hundreds of workers lost their jobs, but Bain and Romney weren't crying: They'd made more than $100 million on a $5 million investment.

To recap: Romney, who has compared the devilish federal debt to a "nightmare" home mortgage that is "adjustable, no-money down and assigned to our children," took over Ampad with essentially no money down, saddled the firm with a nightmare debt and assigned the crushing interest payments not to Bain but to the children of Ampad's workers, who would be left holding the note long after Romney fled the scene. The mortgage analogy is so obvious, in fact, that even Romney himself has made it. He once described Bain's debt-fueled strategy as "using the equivalent of a mortgage to leverage up our investment."

Romney has always kept his distance from the real-life consequences of his profiteering. At one point during Bain's looting of Ampad, a worker named Randy Johnson sent a handwritten letter to Romney, asking him to intervene to save an Ampad factory in Marion, Indiana. In a sterling demonstration of manliness and willingness to face a difficult conversation, Romney, who had just lost his race for the Senate in Massachusetts, wrote Johnson that he was "sorry," but his lawyers had advised him not to get involved. (So much for the candidate who insists that his way is always to "fight to save every job.")

This is typical Romney, who consistently adopts a public posture of having been above the fray, with no blood on his hands from any of the deals he personally engineered. "I never actually ran one of our investments," he says in Turnaround. "That was left to management."

In reality, though, Romney was unquestionably the decider at Bain. "I insisted on having almost dictatorial powers," he bragged years after the Ampad deal. Over the years, colleagues would anonymously whisper stories about Mitt the Boss to the press, describing him as cunning, manipulative and a little bit nuts, with "an ability to identify people's insecurities and exploit them for his own benefit." One former Bain employee said that Romney would screw around with bonuses in small amounts, just to mess with people: He would give $3 million to one, $3.1 million to another and $2.9 million to a third, just to keep those below him on edge.

The private equity business in the early Nineties was dominated by a handful of takeover firms, from the spooky and politically connected Carlyle Group (a favorite subject of conspiracy-theory lit, with its connections to right-wingers like Donald Rumsfeld and George H.W. Bush) to the equally spooky Democrat-leaning assholes at the Blackstone Group. But even among such a colorful cast of characters, Bain had a reputation on Wall Street for secrecy and extreme weirdness - "the KGB of consulting." Its employees, known for their Mormonish uniform of white shirts and red power ties, were dubbed "Bainies" by other Wall Streeters, a rip on the fanatical "Moonies." The firm earned the name thanks to its idiotically adolescent Spy Kids culture, in which these glorified slumlords used code names, didn't carry business cards and even sang "company songs" to boost morale.

The seemingly religious flavor of Bain's culture smacks of the generally cultish ethos on Wall Street, in which all sorts of ethically questionable behaviors are justified as being necessary in service of the church of making money. Romney belongs to a true-believer subset within that cult, with a revolutionary's faith in the wisdom of the pure free market, in which destroying companies and sucking the value out of them for personal gain is part of the greater good, and governments should "stand aside and allow the creative destruction inherent in the free economy."

That cultlike zeal helps explains why Romney takes such a curiously unapologetic approach to his own flip-flopping. His infamous changes of stance are not little wispy ideological alterations of a few degrees here or there - they are perfect and absolute mathematical reversals, as in "I believe that abortion should be safe and legal in this country" and "I am firmly pro-life." Yet unlike other politicians, who at least recognize that saying completely contradictory things presents a political problem, Romney seems genuinely puzzled by the public's insistence that he be consistent. "I'm not going to apologize for having changed my mind," he likes to say. It's an attitude that recalls the standard defense offered by Wall Street in the wake of some of its most recent and notorious crimes: Goldman Sachs excused its lying to clients, for example, by insisting that its customers are "sophisticated investors" who should expect to be lied to. "Last time I checked," former Morgan Stanley CEO John Mack sneered after the same scandal, "we were in business to be profitable."

Within the cult of Wall Street that forged Mitt Romney, making money justifies any behavior, no matter how venal. The look on Romney's face when he refuses to apologize says it all: Hey, I'm trying to win an election. We're all grown-ups here. After the Ampad deal, Romney expressed contempt for critics who lived in "fantasy land." "This is the real world," he said, "and in the real world there is nothing wrong with companies trying to compete, trying to stay alive, trying to make money."

In the old days, making money required sharing the wealth: with assembly-line workers, with middle management, with schools and communities, with investors. Even the Gilded Age robber barons, despite their unapologetic efforts to keep workers from getting any rights at all, built America in spite of themselves, erecting railroads and oil wells and telegraph wires. And from the time the monopolists were reined in with antitrust laws through the days when men like Mitt Romney's dad exited center stage in our economy, the American social contract was pretty consistent: The rich got to stay rich, often filthy rich, but they paid taxes and a living wage and everyone else rose at least a little bit along with them.

But under Romney's business model, leveraging other people's debt means you can carve out big profits for yourself and leave everyone else holding the bag. Despite what Romney claims, the rate of return he provided for Bain's investors over the years wasn't all that great. Romney biographer and Wall Street Journal reporter Brett Arends, who analyzed Bain's performance between 1984 and 1998, concludes that the firm's returns were likely less than 30 percent per year, which happened to track more or less with the stock market's average during that time. "That's how much money you could have made by issuing company bonds and then spending the money picking stocks out of the paper at random," Arends observes. So for all the destruction Romney wreaked on Middle America in the name of "trying to make money," investors could have just plunked their money into traditional stocks and gotten pretty much the same returns.

The only ones who profited in a big way from all the job-killing debt that Romney leveraged were Mitt and his buddies at Bain, along with Wall Street firms like Goldman and Citigroup. Barry Ritholtz, author of Bailout Nation, says the criticisms of Bain about layoffs and meanness miss a more important point, which is that the firm's profit-producing record is absurdly mediocre, especially when set against all the trouble and pain its business model causes. "Bain's fundamental flaw, at least according to the math," Ritholtz writes, "is that they took lots of risk, use immense leverage and charged enormous fees, for performance that was more or less the same as [stock] indexing."

'I'm not a Romney guy, because I'm not a Bain guy," says Lenny Patnode, in an Irish pub in the factory town of Pittsfield, Massachusetts. "But I'm not an Obama guy, either. Just so you know."

I feel bad even asking Patnode about Romney. Big and burly, with white hair and the thick forearms of a man who's stocked a shelf or two in his lifetime, he seems to belong to an era before things like leveraged debt even existed. For 38 years, Patnode worked for a company called KB Toys in Pittsfield. He was the longest-serving employee in the company's history, opening some of the firm's first mall stores, making some of its canniest product buys ("Tamagotchi pets," he says, beaming, "and Tech-Decks, too"), traveling all over the world to help build an empire that at its peak included 1,300 stores. "There were times when I worked seven days a week, 16 hours a day," he says. "I opened three stores in two months once."

Then in 2000, right before Romney gave up his ownership stake in Bain Capital, the firm targeted KB Toys. The debacle that followed serves as a prime example of the conflict between the old model of American business, built from the ground up with sweat and industry know-how, and the new globalist model, the Romney model, which uses leverage as a weapon of high-speed conquest.

In a typical private-equity fragging, Bain put up a mere $18 million to acquire KB Toys and got big banks to finance the remaining $302 million it needed. Less than a year and a half after the purchase, Bain decided to give itself a gift known as a "dividend recapitalization." The firm induced KB Toys to redeem $121 million in stock and take out more than $66 million in bank loans - $83 million of which went directly into the pockets of Bain's owners and investors, including Romney. "The dividend recap is like borrowing someone else's credit card to take out a cash advance, and then leaving them to pay it off," says Heather Slavkin Corzo, who monitors private equity takeovers as the senior legal policy adviser for the AFL-CIO.

Bain ended up earning a return of at least 370 percent on the deal, while KB Toys fell into bankruptcy, saddled with millions in debt. KB's former parent company, Big Lots, alleged in bankruptcy court that Bain's "unjustified" return on the dividend recap was actually "900 percent in a mere 16 months." Patnode, by contrast, was fired in December 2008, after almost four decades on the job. Like other employees, he didn't get a single day's severance.

I ask Slavkin Corzo what Bain's justification was for the giant dividend recapitalization in the KB Toys acquisition. The question throws her, as though she's surprised anyone would ask for a reason a company like Bain would loot a firm like KB Toys. "It wasn't like, 'Yay, we did a good job, we get a dividend,'" she says with a laugh. "It was like, 'We can do this, so we will.' "

At the time of the KB Toys deal, Romney was a Bain investor and owner, making him a mere beneficiary of the raping and pillaging, rather than its direct organizer. Moreover, KB's demise was hastened by a host of genuine market forces, including competition from video games and cellphones. But there's absolutely no way to look at what Bain did at KB and see anything but a cash grab - one that followed the business model laid out by Romney. Rather than cutting costs and tightening belts, Bain added $300 million in debt to the firm's bottom line while taking out more than $120 million in cash - an outright looting that creditors later described in a lawsuit as "breaking open the piggy bank." What's more, Bain smoothed the deal in typical fashion by giving huge bonuses to the company's top managers as the firm headed toward bankruptcy. CEO Michael Glazer got an incredible $18.4 million, while CFO Robert Feldman received $4.8 million and senior VP Thomas Alfonsi took home $3.3 million.

And what did Bain bring to the table in return for its massive, outsize payout? KB Toys had built a small empire by targeting middle-class buyers with value-priced products. It succeeded mainly because the firm's leaders had a great instinct for what they were making and selling. These were people who had been in the specialty toy business since 1922; collectively, they had millions of man-hours of knowledge about how the industry works and how toy customers behave. KB's president in the Eighties, the late Saul Rubenstein, used to carry around a giant computer printout of the company's inventory, and would fall asleep reading it on the weekends, the pages clasped to his chest. "He knew the name and number of all those toys," his widow, Shirley, says proudly. "He loved toys."

Bain's experience in the toy industry, by contrast, was precisely bupkus. They didn't know a damn thing about the business they had taken over - and they never cared to learn. The firm's entire contribution was $18 million in cash and a huge mound of borrowed money that gave it the power to pull the levers. "The people who came in after - they were never toy people," says Shirley Rubenstein. To make matters worse, former employees say, Bain deluged them with requests for paperwork and reports, forcing them to worry more about the whims of their new bosses than the demands of their customers. "We took our eye off the ball," Patnode says. "And if you take your eye off the ball, you strike out."

In the end, Bain never bothered to come up with a plan for how KB Toys could meet the 21st-century challenges of video games and cellphone gadgets that were the company's ostensible downfall. And that's where Romney's self-touted reputation as a turnaround specialist is a myth. In the Bain model, the actual turnaround isn't necessary. It's just a cover story. It's nice for the private equity firm if it happens, because it makes the acquired company more attractive for resale or an IPO. But it's mostly irrelevant to the success of the takeover model, where huge cash returns are extracted whether the captured firm thrives or not.

"The thing about it is, nobody gets hurt," says Patnode. "Except the people who worked here."

Romney was a prime mover in the radical social and political transformation that was cooked up by Wall Street beginning in the 1980s. In fact, you can trace the whole history of the modern age of financialization just by following the highly specific corner of the economic universe inhabited by the leveraged buyout business, where Mitt Romney thrived. If you look at the number of leveraged buyouts dating back two or three decades, you see a clear pattern: Takeovers rose sharply with each of Wall Street's great easy-money schemes, then plummeted just as sharply after each of those scams crashed and burned, leaving the rest of us with the bill.

In the Eighties, when Romney and Bain were cutting their teeth in the LBO business, the primary magic trick involved the junk bonds pioneered by convicted felon Mike Milken, which allowed firms like Bain to find easy financing for takeovers by using wildly overpriced distressed corporate bonds as collateral. Junk bonds gave the Gordon Gekkos of the world sudden primacy over old-school industrial titans like the Fords and the Rockefellers: For the first time, the ability to make deals became more valuable than the ability to make stuff, and the ability to instantly engineer billions in illusory financing trumped the comparatively slow process of making and selling products for gradual returns.

Romney was right in the middle of this radical change. In fact, according to The Boston Globe - whose in-depth reporting on Romney and Bain has spanned three decades - one of Romney's first LBO deals, and one of his most profitable, involved Mike Milken himself. Bain put down $10 million in cash, got $300 million in financing from Milken and bought a pair of department-store chains, Bealls Brothers and Palais Royal. In what should by now be a familiar outcome, the two chains - which Bain merged into a single outfit called Stage Stores - filed for bankruptcy protection in 2000 under the weight of more than $444 million in debt. As always, Bain took no responsibility for the company's demise. (If you search the public record, you will not find a single instance of Mitt Romney taking responsibility for a company's failure.) Instead, Bain blamed Stage's collapse on "operating problems" that took place three years after Bain cashed out, finishing with a $175 million return on its initial investment of $10 million.

But here's the interesting twist: Romney made the Bealls-Palais deal just as the federal government was launching charges of massive manipulation and insider trading against Milken and his firm, Drexel Burnham Lambert. After what must have been a lengthy and agonizing period of moral soul-searching, however, Romney decided not to kill the deal, despite its shady financing. "We did not say, 'Oh, my goodness, Drexel has been accused of something, not been found guilty,' " Romney told reporters years after the deal. "Should we basically stop the transaction and blow the whole thing up?"

In an even more incredible disregard for basic morality, Romney forged ahead with the deal even though Milken's case was being heard by a federal district judge named Milton Pollack, whose wife, Moselle, happened to be the chairwoman of none other than Palais Royal. In short, one of Romney's first takeover deals was financed by dirty money - and one of the corporate chiefs about to receive a big payout from Bain was married to the judge hearing the case. Although the SEC took no formal action, it issued a sharp criticism, complaining that Romney was allowing Milken's money to have a possible influence over "the administration of justice."

After Milken and his junk bond scheme crashed in the late Eighties, Romney and other takeover artists moved on to Wall Street's next get-rich-quick scheme: the tech-Internet stock bubble. By 1997 and 1998, there were nearly $400 billion in leveraged buyouts a year, as easy money once again gave these financial piracy firms the ammunition they needed to raid companies like KB Toys. Firms like Bain even have a colorful pirate name for the pools of takeover money they raise in advance from pension funds, university endowments and other institutional investors. "They call it dry powder," says Slavkin Corzo, the union adviser.

After the Internet bubble burst and private equity started cashing in on Wall Street's mortgage scam, LBO deals ballooned to almost $900 billion in 2006. Once again, storied companies with long histories and deep regional ties were descended upon by Bain and other pirates, saddled with hundreds of millions in debt, forced to pay huge management fees and "dividend recapitalizations," and ridden into bankruptcy amid waves of layoffs. Established firms like Del Monte, Hertz and Dollar General were all taken over in a "prairie fire of debt" - one even more destructive than the government borrowing that Romney is flogging on the campaign trial. When Hertz was conquered in 2005 by a trio of private equity firms, including the Carlyle Group, the interest payments on its debt soared by a monstrous 80 percent, forcing the company to eliminate a third of its 32,000 jobs.

In 2010, a year after the last round of Hertz layoffs, Carlyle teamed up with Bain to take $500 million out of another takeover target: the parent company of Dunkin' Donuts and Baskin-Robbins. Dunkin' had to take out a $1.25 billion loan to pay a dividend to its new private equity owners. So think of this the next time you go to Dunkin' Donuts for a cup of coffee: A small cup of joe costs about $1.69 in most outlets, which means that for years to come, Dunkin' Donuts will have to sell about 2,011,834 small coffees every month - about $3.4 million - just to meet the interest payments on the loan it took out to pay Bain and Carlyle their little one-time dividend. And that doesn't include the principal on the loan, or the additional millions in debt that Dunkin' has to pay every year to get out from under the $2.4 billion in debt it's now saddled with after having the privilege of being taken over - with borrowed money - by the firm that Romney built.

If you haven't heard much about how takeover deals like Dunkin' and KB Toys work, that's because Mitt Romney and his private equity brethren don't want you to. The new owners of American industry are the polar opposites of the Milton Hersheys and Andrew Carnegies who built this country, commercial titans who longed to leave visible legacies of their accomplishments, erecting hospitals and schools and libraries, sometimes leaving behind thriving towns that bore their names.

The men of the private equity generation want no such thing. "We try to hide religiously," explained Steven Feinberg, the CEO of a takeover firm called Cerberus Capital Management that recently drove one of its targets into bankruptcy after saddling it with $2.3 billion in debt. "If anyone at Cerberus has his picture in the paper and a picture of his apartment, we will do more than fire that person," Feinberg told shareholders in 2007. "We will kill him. The jail sentence will be worth it."

Which brings us to another aspect of Romney's business career that has largely been hidden from voters: His personal fortune would not have been possible without the direct assistance of the U.S. government. The taxpayer-funded subsidies that Romney has received go well beyond the humdrum, backdoor, welfare-sucking that all supposedly self-made free marketeers inevitably indulge in. Not that Romney hasn't done just fine at milking the government when it suits his purposes, the most obvious instance being the incredible $1.5 billion in aid he siphoned out of the U.S. Treasury as head of the 2002 Winter Olympics in Salt Lake - a sum greater than all federal spending for the previous seven U.S. Olympic games combined. Romney, the supposed fiscal conservative, blew through an average of $625,000 in taxpayer money per athlete - an astounding increase of 5,582 percent over the $11,000 average at the 1984 games in Los Angeles. In 1993, right as he was preparing to run for the Senate, Romney also engineered a government deal worth at least $10 million for Bain's consulting firm, when it was teetering on the edge of bankruptcy. (See "The Federal Bailout That Saved Romney," page 52.)

But the way Romney most directly owes his success to the government is through the structure of the tax code. The entire business of leveraged buyouts wouldn't be possible without a provision in the federal code that allows companies like Bain to deduct the interest on the debt they use to acquire and loot their targets. This is the same universally beloved tax deduction you can use to write off your mortgage interest payments, so tampering with it is considered political suicide - it's been called the "third rail of tax reform." So the Romney who routinely rails against the national debt as some kind of child-killing "mortgage" is the same man who spent decades exploiting a tax deduction specifically designed for mortgage holders in order to bilk every dollar he could out of U.S. businesses before burning them to the ground.

Because minus that tax break, Romney's debt-based takeovers would have been unsustainably expensive. Before Lynn Turner became chief accountant of the SEC, where he reviewed filings on takeover deals, he crunched the numbers on leveraged buyouts as an accountant at a Big Four auditing firm. "In the majority of these deals," Turner says, "the tax deduction has a big enough impact on the bottom line that the takeover wouldn't work without it."

Thanks to the tax deduction, in other words, the government actually incentivizes the kind of leverage-based takeovers that Romney built his fortune on. Romney the businessman built his career on two things that Romney the candidate decries: massive debt and dumb federal giveaways. "I don't know what Romney would be doing but for debt and its tax-advantaged position in the tax code," says a prominent Wall Street lawyer, "but he wouldn't be fabulously wealthy."

Adding to the hypocrisy, the money that Romney personally pocketed on Bain's takeover deals was usually taxed not as income, but either as capital gains or as "carried interest," both of which are capped at a maximum rate of 15 percent. In addition, reporters have uncovered plenty of evidence that Romney takes full advantage of offshore tax havens: He has an interest in at least 12 Bain funds, worth a total of $30 million, that are based in the Cayman Islands; he has reportedly used a squirrelly tax shelter known as a "blocker corporation" that cheats taxpayers out of some $100 million a year; and his wife, Ann, had a Swiss bank account worth $3 million. As a private equity pirate, Romney pays less than half the tax rate of most American executives - less, even, than teachers, firefighters, cops and nurses. Asked about the fact that he paid a tax rate of only 13.9 percent on income of $21.7 million in 2010, Romney responded testily that the massive windfall he enjoys from exploiting the tax code is "entirely legal and fair."

Essentially, Romney got rich in a business that couldn't exist without a perverse tax break, and he got to keep double his earnings because of another loophole - a pair of bureaucratic accidents that have not only teamed up to threaten us with a Mitt Romney presidency but that make future Romneys far more likely. "Those two tax rules distort the economics of private equity investments, making them much more lucrative than they should be," says Rebecca Wilkins, senior counsel at the Center for Tax Justice. "So we get more of that activity than the market would support on its own."

Listen to Mitt Romney speak, and see if you can notice what's missing. This is a man who grew up in Michigan, went to college in California, walked door to door through the streets of southern France as a missionary and was a governor of Massachusetts, the home of perhaps the most instantly recognizable, heavily accented English this side of Edinburgh. Yet not a trace of any of these places is detectable in Romney's diction. None of the people in any of those places bled in and left a mark on the man.

Romney is a man from nowhere. In his post-regional attitude, he shares something with his campaign opponent, Barack Obama, whose background is a similarly jumbled pastiche of regionally nonspecific non-identity. But in the way he bounced around the world as a half-orphaned child, Obama was more like an involuntary passenger in the demographic revolution reshaping the planet than one of its leaders.

Romney, on the other hand, is a perfect representative of one side of the ominous cultural divide that will define the next generation, not just here in America but all over the world. Forget about the Southern strategy, blue versus red, swing states and swing voters - all of those political cliches are quaint relics of a less threatening era that is now part of our past, or soon will be. The next conflict defining us all is much more unnerving.

That conflict will be between people who live somewhere, and people who live nowhere. It will be between people who consider themselves citizens of actual countries, to which they have patriotic allegiance, and people to whom nations are meaningless, who live in a stateless global archipelago of privilege - a collection of private schools, tax havens and gated residential communities with little or no connection to the outside world.

Mitt Romney isn't blue or red. He's an archipelago man. That's a big reason that voters have been slow to warm up to him. From LBJ to Bill Clinton to George W. Bush to Sarah Palin, Americans like their politicians to sound like they're from somewhere, to be human symbols of our love affair with small towns, the girl next door, the little pink houses of Mellencamp myth. Most of those mythical American towns grew up around factories - think chocolate bars from Hershey, baseball bats from Louisville, cereals from Battle Creek. Deep down, what scares voters in both parties the most is the thought that these unique and vital places are vanishing or eroding - overrun by immigrants or the forces of globalism or both, with giant Walmarts descending like spaceships to replace the corner grocer, the family barber and the local hardware store, and 1,000 cable channels replacing the school dance and the gossip at the local diner.

Obama ran on "change" in 2008, but Mitt Romney represents a far more real and seismic shift in the American landscape. Romney is the frontman and apostle of an economic revolution, in which transactions are manufactured instead of products, wealth is generated without accompanying prosperity, and Cayman Islands partnerships are lovingly erected and nurtured while American communities fall apart. The entire purpose of the business model that Romney helped pioneer is to move money into the archipelago from the places outside it, using massive amounts of taxpayer-subsidized debt to enrich a handful of billionaires. It's a vision of society that's crazy, vicious and almost unbelievably selfish, yet it's running for president, and it has a chance of winning. Perhaps that change is coming whether we like it or not. Perhaps Mitt Romney is the best man to manage the transition. But it seems a little early to vote for that kind of wholesale surrender.

The great criticism of Mitt Romney, from both sides of the aisle, has always been that he doesn't stand for anything. He's a flip-flopper, they say, a lightweight, a cardboard opportunist who'll say anything to get elected.

The critics couldn't be more wrong. Mitt Romney is no tissue-paper man. He's closer to being a revolutionary, a backward-world version of Che or Trotsky, with tweezed nostrils instead of a beard, a half-Windsor instead of a leather jerkin. His legendary flip-flops aren't the lies of a bumbling opportunist - they're the confident prevarications of a man untroubled by misleading the nonbeliever in pursuit of a single, all-consuming goal. Romney has a vision, and he's trying for something big: We've just been too slow to sort out what it is, just as we've been slow to grasp the roots of the radical economic changes that have swept the country in the last generation.

The incredible untold story of the 2012 election so far is that Romney's run has been a shimmering pearl of perfect political hypocrisy, which he's somehow managed to keep hidden, even with thousands of cameras following his every move. And the drama of this rhetorical high-wire act was ratcheted up even further when Romney chose his running mate, Rep. Paul Ryan of Wisconsin - like himself, a self-righteously anal, thin-lipped, Whitest Kids U Know penny pincher who'd be honored to tell Oliver Twist there's no more soup left. By selecting Ryan, Romney, the hard-charging, chameleonic champion of a disgraced-yet-defiant Wall Street, officially succeeded in moving the battle lines in the 2012 presidential race.

Like John McCain four years before, Romney desperately needed a vice-presidential pick that would change the game. But where McCain bet on a combustive mix of clueless novelty and suburban sexual tension named Sarah Palin, Romney bet on an idea. He said as much when he unveiled his choice of Ryan, the author of a hair-raising budget-cutting plan best known for its willingness to slash the sacred cows of Medicare and Medicaid. "Paul Ryan has become an intellectual leader of the Republican Party," Romney told frenzied Republican supporters in Norfolk, Virginia, standing before the reliably jingoistic backdrop of a floating warship. "He understands the fiscal challenges facing America: our exploding deficits and crushing debt."

Debt, debt, debt. If the Republican Party had a James Carville, this is what he would have said to win Mitt over, in whatever late-night war room session led to the Ryan pick: "It's the debt, stupid." This is the way to defeat Barack Obama: to recast the race as a jeremiad against debt, something just about everybody who's ever gotten a bill in the mail hates on a primal level.

Last May, in a much-touted speech in Iowa, Romney used language that was literally inflammatory to describe America's federal borrowing. "A prairie fire of debt is sweeping across Iowa and our nation," he declared. "Every day we fail to act, that fire gets closer to the homes and children we love." Our collective debt is no ordinary problem: According to Mitt, it's going to burn our children alive.

And this is where we get to the hypocrisy at the heart of Mitt Romney. Everyone knows that he is fantastically rich, having scored great success, the legend goes, as a "turnaround specialist," a shrewd financial operator who revived moribund companies as a high-priced consultant for a storied Wall Street private equity firm. But what most voters don't know is the way Mitt Romney actually made his fortune: by borrowing vast sums of money that other people were forced to pay back. This is the plain, stark reality that has somehow eluded America's top political journalists for two consecutive presidential campaigns: Mitt Romney is one of the greatest and most irresponsible debt creators of all time. In the past few decades, in fact, Romney has piled more debt onto more unsuspecting companies, written more gigantic checks that other people have to cover, than perhaps all but a handful of people on planet Earth.

By making debt the centerpiece of his campaign, Romney was making a calculated bluff of historic dimensions - placing a massive all-in bet on the rank incompetence of the American press corps. The result has been a brilliant comedy: A man makes a $250 million fortune loading up companies with debt and then extracting million-dollar fees from those same companies, in exchange for the generous service of telling them who needs to be fired in order to finance the debt payments he saddled them with in the first place. That same man then runs for president riding an image of children roasting on flames of debt, choosing as his running mate perhaps the only politician in America more pompous and self-righteous on the subject of the evils of borrowed money than the candidate himself. If Romney pulls off this whopper, you'll have to tip your hat to him: No one in history has ever successfully run for president riding this big of a lie. It's almost enough to make you think he really is qualified for the White House.

The unlikeliness of Romney's gambit isn't simply a reflection of his own artlessly unapologetic mindset - it stands as an emblem for the resiliency of the entire sociopathic Wall Street set he represents. Four years ago, the Mitt Romneys of the world nearly destroyed the global economy with their greed, shortsightedness and - most notably - wildly irresponsible use of debt in pursuit of personal profit. The sight was so disgusting that people everywhere were ready to drop an H-bomb on Lower Manhattan and bayonet the survivors. But today that same insane greed ethos, that same belief in the lunatic pursuit of instant borrowed millions - it's dusted itself off, it's had a shave and a shoeshine, and it's back out there running for president.

Mitt Romney, it turns out, is the perfect frontman for Wall Street's greed revolution. He's not a two-bit, shifty-eyed huckster like Lloyd Blankfein. He's not a sighing, eye-rolling, arrogant jerkwad like Jamie Dimon. But Mitt believes the same things those guys believe: He's been right with them on the front lines of the financialization revolution, a decades-long campaign in which the old, simple, let's-make-stuff-and-sell-it manufacturing economy was replaced with a new, highly complex, let's-take-stuff-and-trash-it financial economy. Instead of cars and airplanes, we built swaps, CDOs and other toxic financial products. Instead of building new companies from the ground up, we took out massive bank loans and used them to acquire existing firms, liquidating every asset in sight and leaving the target companies holding the note. The new borrow-and-conquer economy was morally sanctified by an almost religious faith in the grossly euphemistic concept of "creative destruction," and amounted to a total abdication of collective responsibility by America's rich, whose new thing was making assloads of money in ever-shorter campaigns of economic conquest, sending the proceeds offshore, and shrugging as the great towns and factories their parents and grandparents built were shuttered and boarded up, crushed by a true prairie fire of debt.

Mitt Romney - a man whose own father built cars and nurtured communities, and was one of the old-school industrial anachronisms pushed aside by the new generation's wealth grab - has emerged now to sell this make-nothing, take-everything, screw-everyone ethos to the world. He's Gordon Gekko, but a new and improved version, with better PR - and a bigger goal. A takeover artist all his life, Romney is now trying to take over America itself. And if his own history is any guide, we'll all end up paying for the acquisition.

Willard "Mitt" Romney's background in many ways suggests a man who was born to be president - disgustingly rich from birth, raised in prep schools, no early exposure to minorities outside of maids, a powerful daddy to clean up his missteps, and timely exemptions from military service. In Romney's bio there are some eerie early-life similarities to other recent presidential figures. (Is America really ready for another Republican president who was a prep-school cheerleader?) And like other great presidential double-talkers such as Bill Clinton and George W. Bush, Romney has shown particular aptitude in the area of telling multiple factual versions of his own life story.

"I longed in many respects to actually be in Vietnam and be representing our country there," he claimed years after the war. To a different audience, he said, "I was not planning on signing up for the military. It was not my desire to go off and serve in Vietnam."

Like John F. Kennedy and George W. Bush, men whose way into power was smoothed by celebrity fathers but who rebelled against their parental legacy as mature politicians, Mitt Romney's career has been both a tribute to and a repudiation of his famous father. George Romney in the 1950s became CEO of American Motors Corp., made a modest fortune betting on energy efficiency in an age of gas guzzlers and ended up serving as governor of the state of Michigan only two generations removed from the Romney clan's tradition of polygamy. For Mitt, who grew up worshipping his tall, craggily handsome, politically moderate father, life was less rocky: Cranbrook prep school in suburban Detroit, followed by Stanford in the Sixties, a missionary term in which he spent two and a half years trying (as he said) to persuade the French to "give up your wine," and Harvard Business School in the Seventies. Then, faced with making a career choice, Mitt chose an odd one: Already married and a father of two, he left Harvard and eschewed both politics and the law to enter the at-the-time unsexy world of financial consulting.

"When you get out of a place like Harvard, you can do anything - at least in the old days you could," says a prominent corporate lawyer on Wall Street who is familiar with Romney's career. "But he comes out, he not only has a Harvard Business School degree, he's got a national pedigree with his name. He could have done anything - but what does he do? He says, 'I'm going to spend my life loading up distressed companies with debt.' "

Romney started off at the Boston Consulting Group, where he showed an aptitude for crunching numbers and glad-handing clients. Then, in 1977, he joined a young entrepreneur named Bill Bain at a firm called Bain & Company, where he worked for six years before being handed the reins of a new firm-within-a-firm called Bain Capital.

In Romney's version of the tale, Bain Capital - which evolved into what is today known as a private equity firm - specialized in turning around moribund companies (Romney even wrote a book called Turnaround that complements his other nauseatingly self-complimentary book, No Apology) and helped create the Staples office-supply chain. On the campaign trail, Romney relentlessly trades on his own self-perpetuated reputation as a kind of altruistic rescuer of failing enterprises, never missing an opportunity to use the word "help" or "helped" in his description of what he and Bain did for companies. He might, for instance, describe himself as having been "deeply involved in helping other businesses" or say he "helped create tens of thousands of jobs."

The reality is that toward the middle of his career at Bain, Romney made a fateful strategic decision: He moved away from creating companies like Staples through venture capital schemes, and toward a business model that involved borrowing huge sums of money to take over existing firms, then extracting value from them by force. He decided, as he later put it, that "there's a lot greater risk in a startup than there is in acquiring an existing company." In the Eighties, when Romney made this move, this form of financial piracy became known as a leveraged buyout, and it achieved iconic status thanks to Gordon Gekko in Wall Street. Gekko's business strategy was essentially identical to the Romney-Bain model, only Gekko called himself a "liberator" of companies instead of a "helper."

Here's how Romney would go about "liberating" a company: A private equity firm like Bain typically seeks out floundering businesses with good cash flows. It then puts down a relatively small amount of its own money and runs to a big bank like Goldman Sachs or Citigroup for the rest of the financing. (Most leveraged buyouts are financed with 60 to 90 percent borrowed cash.) The takeover firm then uses that borrowed money to buy a controlling stake in the target company, either with or without its consent. When an LBO is done without the consent of the target, it's called a hostile takeover; such thrilling acts of corporate piracy were made legend in the Eighties, most notably the 1988 attack by notorious corporate raiders Kohlberg Kravis Roberts against RJR Nabisco, a deal memorialized in the book Barbarians at the Gate.

Romney and Bain avoided the hostile approach, preferring to secure the cooperation of their takeover targets by buying off a company's management with lucrative bonuses. Once management is on board, the rest is just math. So if the target company is worth $500 million, Bain might put down $20 million of its own cash, then borrow $350 million from an investment bank to take over a controlling stake.

But here's the catch. When Bain borrows all of that money from the bank, it's the target company that ends up on the hook for all of the debt.

Now your troubled firm - let's say you make tricycles in Alabama - has been taken over by a bunch of slick Wall Street dudes who kicked in as little as five percent as a down payment. So in addition to whatever problems you had before, Tricycle Inc. now owes Goldman or Citigroup $350 million. With all that new debt service to pay, the company's bottom line is suddenly untenable: You almost have to start firing people immediately just to get your costs down to a manageable level.

"That interest," says Lynn Turner, former chief accountant of the Securities and Exchange Commission, "just sucks the profit out of the company."

Fortunately, the geniuses at Bain who now run the place are there to help tell you whom to fire. And for the service it performs cutting your company's costs to help you pay off the massive debt that it, Bain, saddled your company with in the first place, Bain naturally charges a management fee, typically millions of dollars a year. So Tricycle Inc. now has two gigantic new burdens it never had before Bain Capital stepped into the picture: tens of millions in annual debt service, and millions more in "management fees." Since the initial acquisition of Tricycle Inc. was probably greased by promising the company's upper management lucrative bonuses, all that pain inevitably comes out of just one place: the benefits and payroll of the hourly workforce.

Once all that debt is added, one of two things can happen. The company can fire workers and slash benefits to pay off all its new obligations to Goldman Sachs and Bain, leaving it ripe to be resold by Bain at a huge profit. Or it can go bankrupt - this happens after about seven percent of all private equity buyouts - leaving behind one or more shuttered factory towns. Either way, Bain wins. By power-sucking cash value from even the most rapidly dying firms, private equity raiders like Bain almost always get their cash out before a target goes belly up.

This business model wasn't really "helping," of course - and it wasn't new. Fans of mob movies will recognize what's known as the "bust-out," in which a gangster takes over a restaurant or sporting goods store and then monetizes his investment by running up giant debts on the company's credit line. (Think Paulie buying all those cases of Cutty Sark in Goodfellas.) When the note comes due, the mobster simply torches the restaurant and collects the insurance money. Reduced to their most basic level, the leveraged buyouts engineered by Romney followed exactly the same business model. "It's the bust-out," one Wall Street trader says with a laugh. "That's all it is."

Private equity firms aren't necessarily evil by definition. There are many stories of successful turnarounds fueled by private equity, often involving multiple floundering businesses that are rolled into a single entity, eliminating duplicative overhead. Experian, the giant credit-rating tyrant, was acquired by Bain in the Nineties and went on to become an industry leader.

But there's a key difference between private equity firms and the businesses that were America's original industrial cornerstones, like the elder Romney's AMC. Everyone had a stake in the success of those old businesses, which spread prosperity by putting people to work. But even private equity's most enthusiastic adherents have difficulty explaining its benefit to society. Marc Wolpow, a former Bain colleague of Romney's, told reporters during Mitt's first Senate run that Romney erred in trying to sell his business as good for everyone. "I believed he was making a mistake by framing himself as a job creator," said Wolpow. "That was not his or Bain's or the industry's primary objective. The objective of the LBO business is maximizing returns for investors." When it comes to private equity, American workers - not to mention their families and communities - simply don't enter into the equation.

Take a typical Bain transaction involving an Indiana-based company called American Pad and Paper. Bain bought Ampad in 1992 for just $5 million, financing the rest of the deal with borrowed cash. Within three years, Ampad was paying $60 million in annual debt payments, plus an additional $7 million in management fees. A year later, Bain led Ampad to go public, cashed out about $50 million in stock for itself and its investors, charged the firm $2 million for arranging the IPO and pocketed another $5 million in "management" fees. Ampad wound up going bankrupt, and hundreds of workers lost their jobs, but Bain and Romney weren't crying: They'd made more than $100 million on a $5 million investment.

To recap: Romney, who has compared the devilish federal debt to a "nightmare" home mortgage that is "adjustable, no-money down and assigned to our children," took over Ampad with essentially no money down, saddled the firm with a nightmare debt and assigned the crushing interest payments not to Bain but to the children of Ampad's workers, who would be left holding the note long after Romney fled the scene. The mortgage analogy is so obvious, in fact, that even Romney himself has made it. He once described Bain's debt-fueled strategy as "using the equivalent of a mortgage to leverage up our investment."

Romney has always kept his distance from the real-life consequences of his profiteering. At one point during Bain's looting of Ampad, a worker named Randy Johnson sent a handwritten letter to Romney, asking him to intervene to save an Ampad factory in Marion, Indiana. In a sterling demonstration of manliness and willingness to face a difficult conversation, Romney, who had just lost his race for the Senate in Massachusetts, wrote Johnson that he was "sorry," but his lawyers had advised him not to get involved. (So much for the candidate who insists that his way is always to "fight to save every job.")

This is typical Romney, who consistently adopts a public posture of having been above the fray, with no blood on his hands from any of the deals he personally engineered. "I never actually ran one of our investments," he says in Turnaround. "That was left to management."

In reality, though, Romney was unquestionably the decider at Bain. "I insisted on having almost dictatorial powers," he bragged years after the Ampad deal. Over the years, colleagues would anonymously whisper stories about Mitt the Boss to the press, describing him as cunning, manipulative and a little bit nuts, with "an ability to identify people's insecurities and exploit them for his own benefit." One former Bain employee said that Romney would screw around with bonuses in small amounts, just to mess with people: He would give $3 million to one, $3.1 million to another and $2.9 million to a third, just to keep those below him on edge.

The private equity business in the early Nineties was dominated by a handful of takeover firms, from the spooky and politically connected Carlyle Group (a favorite subject of conspiracy-theory lit, with its connections to right-wingers like Donald Rumsfeld and George H.W. Bush) to the equally spooky Democrat-leaning assholes at the Blackstone Group. But even among such a colorful cast of characters, Bain had a reputation on Wall Street for secrecy and extreme weirdness - "the KGB of consulting." Its employees, known for their Mormonish uniform of white shirts and red power ties, were dubbed "Bainies" by other Wall Streeters, a rip on the fanatical "Moonies." The firm earned the name thanks to its idiotically adolescent Spy Kids culture, in which these glorified slumlords used code names, didn't carry business cards and even sang "company songs" to boost morale.

The seemingly religious flavor of Bain's culture smacks of the generally cultish ethos on Wall Street, in which all sorts of ethically questionable behaviors are justified as being necessary in service of the church of making money. Romney belongs to a true-believer subset within that cult, with a revolutionary's faith in the wisdom of the pure free market, in which destroying companies and sucking the value out of them for personal gain is part of the greater good, and governments should "stand aside and allow the creative destruction inherent in the free economy."

That cultlike zeal helps explains why Romney takes such a curiously unapologetic approach to his own flip-flopping. His infamous changes of stance are not little wispy ideological alterations of a few degrees here or there - they are perfect and absolute mathematical reversals, as in "I believe that abortion should be safe and legal in this country" and "I am firmly pro-life." Yet unlike other politicians, who at least recognize that saying completely contradictory things presents a political problem, Romney seems genuinely puzzled by the public's insistence that he be consistent. "I'm not going to apologize for having changed my mind," he likes to say. It's an attitude that recalls the standard defense offered by Wall Street in the wake of some of its most recent and notorious crimes: Goldman Sachs excused its lying to clients, for example, by insisting that its customers are "sophisticated investors" who should expect to be lied to. "Last time I checked," former Morgan Stanley CEO John Mack sneered after the same scandal, "we were in business to be profitable."

Within the cult of Wall Street that forged Mitt Romney, making money justifies any behavior, no matter how venal. The look on Romney's face when he refuses to apologize says it all: Hey, I'm trying to win an election. We're all grown-ups here. After the Ampad deal, Romney expressed contempt for critics who lived in "fantasy land." "This is the real world," he said, "and in the real world there is nothing wrong with companies trying to compete, trying to stay alive, trying to make money."

In the old days, making money required sharing the wealth: with assembly-line workers, with middle management, with schools and communities, with investors. Even the Gilded Age robber barons, despite their unapologetic efforts to keep workers from getting any rights at all, built America in spite of themselves, erecting railroads and oil wells and telegraph wires. And from the time the monopolists were reined in with antitrust laws through the days when men like Mitt Romney's dad exited center stage in our economy, the American social contract was pretty consistent: The rich got to stay rich, often filthy rich, but they paid taxes and a living wage and everyone else rose at least a little bit along with them.

But under Romney's business model, leveraging other people's debt means you can carve out big profits for yourself and leave everyone else holding the bag. Despite what Romney claims, the rate of return he provided for Bain's investors over the years wasn't all that great. Romney biographer and Wall Street Journal reporter Brett Arends, who analyzed Bain's performance between 1984 and 1998, concludes that the firm's returns were likely less than 30 percent per year, which happened to track more or less with the stock market's average during that time. "That's how much money you could have made by issuing company bonds and then spending the money picking stocks out of the paper at random," Arends observes. So for all the destruction Romney wreaked on Middle America in the name of "trying to make money," investors could have just plunked their money into traditional stocks and gotten pretty much the same returns.

The only ones who profited in a big way from all the job-killing debt that Romney leveraged were Mitt and his buddies at Bain, along with Wall Street firms like Goldman and Citigroup. Barry Ritholtz, author of Bailout Nation, says the criticisms of Bain about layoffs and meanness miss a more important point, which is that the firm's profit-producing record is absurdly mediocre, especially when set against all the trouble and pain its business model causes. "Bain's fundamental flaw, at least according to the math," Ritholtz writes, "is that they took lots of risk, use immense leverage and charged enormous fees, for performance that was more or less the same as [stock] indexing."

'I'm not a Romney guy, because I'm not a Bain guy," says Lenny Patnode, in an Irish pub in the factory town of Pittsfield, Massachusetts. "But I'm not an Obama guy, either. Just so you know."

I feel bad even asking Patnode about Romney. Big and burly, with white hair and the thick forearms of a man who's stocked a shelf or two in his lifetime, he seems to belong to an era before things like leveraged debt even existed. For 38 years, Patnode worked for a company called KB Toys in Pittsfield. He was the longest-serving employee in the company's history, opening some of the firm's first mall stores, making some of its canniest product buys ("Tamagotchi pets," he says, beaming, "and Tech-Decks, too"), traveling all over the world to help build an empire that at its peak included 1,300 stores. "There were times when I worked seven days a week, 16 hours a day," he says. "I opened three stores in two months once."

Then in 2000, right before Romney gave up his ownership stake in Bain Capital, the firm targeted KB Toys. The debacle that followed serves as a prime example of the conflict between the old model of American business, built from the ground up with sweat and industry know-how, and the new globalist model, the Romney model, which uses leverage as a weapon of high-speed conquest.

In a typical private-equity fragging, Bain put up a mere $18 million to acquire KB Toys and got big banks to finance the remaining $302 million it needed. Less than a year and a half after the purchase, Bain decided to give itself a gift known as a "dividend recapitalization." The firm induced KB Toys to redeem $121 million in stock and take out more than $66 million in bank loans - $83 million of which went directly into the pockets of Bain's owners and investors, including Romney. "The dividend recap is like borrowing someone else's credit card to take out a cash advance, and then leaving them to pay it off," says Heather Slavkin Corzo, who monitors private equity takeovers as the senior legal policy adviser for the AFL-CIO.

Bain ended up earning a return of at least 370 percent on the deal, while KB Toys fell into bankruptcy, saddled with millions in debt. KB's former parent company, Big Lots, alleged in bankruptcy court that Bain's "unjustified" return on the dividend recap was actually "900 percent in a mere 16 months." Patnode, by contrast, was fired in December 2008, after almost four decades on the job. Like other employees, he didn't get a single day's severance.

I ask Slavkin Corzo what Bain's justification was for the giant dividend recapitalization in the KB Toys acquisition. The question throws her, as though she's surprised anyone would ask for a reason a company like Bain would loot a firm like KB Toys. "It wasn't like, 'Yay, we did a good job, we get a dividend,'" she says with a laugh. "It was like, 'We can do this, so we will.' "

At the time of the KB Toys deal, Romney was a Bain investor and owner, making him a mere beneficiary of the raping and pillaging, rather than its direct organizer. Moreover, KB's demise was hastened by a host of genuine market forces, including competition from video games and cellphones. But there's absolutely no way to look at what Bain did at KB and see anything but a cash grab - one that followed the business model laid out by Romney. Rather than cutting costs and tightening belts, Bain added $300 million in debt to the firm's bottom line while taking out more than $120 million in cash - an outright looting that creditors later described in a lawsuit as "breaking open the piggy bank." What's more, Bain smoothed the deal in typical fashion by giving huge bonuses to the company's top managers as the firm headed toward bankruptcy. CEO Michael Glazer got an incredible $18.4 million, while CFO Robert Feldman received $4.8 million and senior VP Thomas Alfonsi took home $3.3 million.

And what did Bain bring to the table in return for its massive, outsize payout? KB Toys had built a small empire by targeting middle-class buyers with value-priced products. It succeeded mainly because the firm's leaders had a great instinct for what they were making and selling. These were people who had been in the specialty toy business since 1922; collectively, they had millions of man-hours of knowledge about how the industry works and how toy customers behave. KB's president in the Eighties, the late Saul Rubenstein, used to carry around a giant computer printout of the company's inventory, and would fall asleep reading it on the weekends, the pages clasped to his chest. "He knew the name and number of all those toys," his widow, Shirley, says proudly. "He loved toys."

Bain's experience in the toy industry, by contrast, was precisely bupkus. They didn't know a damn thing about the business they had taken over - and they never cared to learn. The firm's entire contribution was $18 million in cash and a huge mound of borrowed money that gave it the power to pull the levers. "The people who came in after - they were never toy people," says Shirley Rubenstein. To make matters worse, former employees say, Bain deluged them with requests for paperwork and reports, forcing them to worry more about the whims of their new bosses than the demands of their customers. "We took our eye off the ball," Patnode says. "And if you take your eye off the ball, you strike out."

In the end, Bain never bothered to come up with a plan for how KB Toys could meet the 21st-century challenges of video games and cellphone gadgets that were the company's ostensible downfall. And that's where Romney's self-touted reputation as a turnaround specialist is a myth. In the Bain model, the actual turnaround isn't necessary. It's just a cover story. It's nice for the private equity firm if it happens, because it makes the acquired company more attractive for resale or an IPO. But it's mostly irrelevant to the success of the takeover model, where huge cash returns are extracted whether the captured firm thrives or not.

"The thing about it is, nobody gets hurt," says Patnode. "Except the people who worked here."