SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

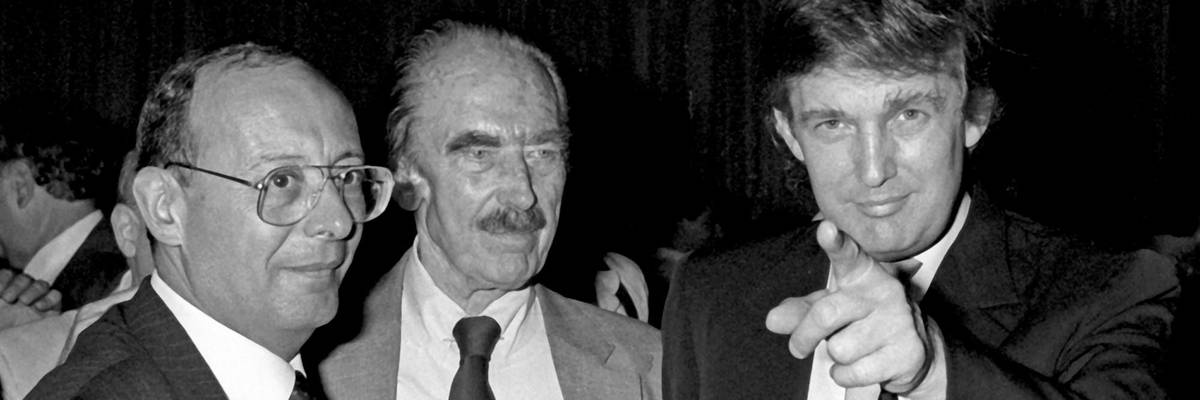

There is no statute of limitations on the complicated con job that The New York Times laid out in its huge, document-laden investigation of Donald Trump's finances.

Trump and his father, real estate developer Fred Trump, used some accounting techniques that look a lot like civil tax fraud. If it is, that could lead to payments of up to 75 percent of the amount underpaid. Trump and his siblings could be forced to surrender, or "disgorge," many millions of dollars -- perhaps hundreds of millions -- in back taxes, fines and penalties to New York state alone.

The Times describes decades of what is politely called "creative accounting." Though the means were complicated, the purpose wasn't: Fred transferred $1 billion to his children, The Times estimates, and paid roughly 5 percent in estate taxes instead of the then-standard 55 percent.

How did they do this? First, the Trumps dramatically undervalued their property, which low-balled the amount of tax they had to pay. They also allegedly devised a whole other kind of fraud, according to The Times, padding virtually all maintenance invoices, so that Fred could list payments to his children as business expenses instead of taxable gifts.

These inflated bills also allowed the Trumps to increase the rents that they charged the low-income tenants in their government-subsidized housing developments. Tenants who could ill afford the rent hikes.

Just as serious -- if not qualifying as civil tax fraud -- is the fraud Donald Trump perpetrated on the American public. As a stripling golden-haired playboy, Trump presented his father's wealth as his own. He then used this claim to create an inflated impression of his own success and, ultimately, made it the basis of his presidential campaign.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it. Tax advisers routinely help clients toward this goal -- mainly in ways that are legal. They see to it that their clients make annual gifts to their children and grandchildren up to the amounts exempt from gift taxes. When the clients pass to their eternal reward, these amounts are then excluded when tallying estate taxes.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it.

There are many other ways to avoid paying the government. Tax advisers, for example, see to it that clients, instead of making gifts to family members for tuition, pay the schools directly. The advisers make sure that clients make maximum use of their tax loss "carryforwards," so that the losses are spread over future years -- and offset any future gains.

And that's not counting the techniques that will put clients under the Internal Revenue Service microscope, like offshore investments and family limited partnerships. Advisers sometimes devise extremely sophisticated write-offs. Trump's sound relatively simple.

Real estate has unique tax rules since, like art, it has to be appraised. You can't definitively say what a building on East 57th Street in Manhattan is worth in the same way that you can quote the price of a share of IBM stock. The appraisal will determine the property's value and, thus, the taxes you owe on your ownership and transfer of the property.

The IRS tries to ensure these appraisals are independent. But you can only go so far. The Trumps, according to The Times account, got themselves an extraordinarily friendly appraiser.

Another tactic they relied on involves control of the partnerships through which real estate is often owned. When you determine the value of an interest in a partnership, the interest is worth less -- it's valued at a discount -- if it comes without control. The Trumps arranged ownership of their properties so that Fred got the discount. Because his interests in his properties were assigned a lower value, he paid less tax on it.

There are parts of this con job for which our president will never be called to account. No one will go to jail for the tax schemes.

There were reportedly other Trump tax reduction techniques. Fred Trump didn't just put his children on his payroll so he could claim his payments to them as business expenses. He also made his children the holders of his property mortgages, rather than working with conventional lenders. His mortgage payments on his buildings went to his kids.

In addition, instead of transferring property interests openly to his children, he transferred them to trusts that covertly benefited them. He extended loans, especially loans to Donald, that were never repaid. He sold property to Donald at a price that made the property a gift.

The other long con also masked Fred's help to his children. He was regularly spending large sums buying goods and services from contractors to maintain and improve his properties. So he set up a company, All County Building Supply & Maintenance, controlled by his children. Fred would pay All County instead of paying the contractors directly. But the All County's invoices to Fred were padded by 20 percent or more. The markups went to the Trump children.

Dear Common Dreams reader, The U.S. is on a fast track to authoritarianism like nothing I've ever seen. Meanwhile, corporate news outlets are utterly capitulating to Trump, twisting their coverage to avoid drawing his ire while lining up to stuff cash in his pockets. That's why I believe that Common Dreams is doing the best and most consequential reporting that we've ever done. Our small but mighty team is a progressive reporting powerhouse, covering the news every day that the corporate media never will. Our mission has always been simple: To inform. To inspire. And to ignite change for the common good. Now here's the key piece that I want all our readers to understand: None of this would be possible without your financial support. That's not just some fundraising cliche. It's the absolute and literal truth. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. Will you donate now to help power the nonprofit, independent reporting of Common Dreams? Thank you for being a vital member of our community. Together, we can keep independent journalism alive when it’s needed most. - Craig Brown, Co-founder |

There is no statute of limitations on the complicated con job that The New York Times laid out in its huge, document-laden investigation of Donald Trump's finances.

Trump and his father, real estate developer Fred Trump, used some accounting techniques that look a lot like civil tax fraud. If it is, that could lead to payments of up to 75 percent of the amount underpaid. Trump and his siblings could be forced to surrender, or "disgorge," many millions of dollars -- perhaps hundreds of millions -- in back taxes, fines and penalties to New York state alone.

The Times describes decades of what is politely called "creative accounting." Though the means were complicated, the purpose wasn't: Fred transferred $1 billion to his children, The Times estimates, and paid roughly 5 percent in estate taxes instead of the then-standard 55 percent.

How did they do this? First, the Trumps dramatically undervalued their property, which low-balled the amount of tax they had to pay. They also allegedly devised a whole other kind of fraud, according to The Times, padding virtually all maintenance invoices, so that Fred could list payments to his children as business expenses instead of taxable gifts.

These inflated bills also allowed the Trumps to increase the rents that they charged the low-income tenants in their government-subsidized housing developments. Tenants who could ill afford the rent hikes.

Just as serious -- if not qualifying as civil tax fraud -- is the fraud Donald Trump perpetrated on the American public. As a stripling golden-haired playboy, Trump presented his father's wealth as his own. He then used this claim to create an inflated impression of his own success and, ultimately, made it the basis of his presidential campaign.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it. Tax advisers routinely help clients toward this goal -- mainly in ways that are legal. They see to it that their clients make annual gifts to their children and grandchildren up to the amounts exempt from gift taxes. When the clients pass to their eternal reward, these amounts are then excluded when tallying estate taxes.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it.

There are many other ways to avoid paying the government. Tax advisers, for example, see to it that clients, instead of making gifts to family members for tuition, pay the schools directly. The advisers make sure that clients make maximum use of their tax loss "carryforwards," so that the losses are spread over future years -- and offset any future gains.

And that's not counting the techniques that will put clients under the Internal Revenue Service microscope, like offshore investments and family limited partnerships. Advisers sometimes devise extremely sophisticated write-offs. Trump's sound relatively simple.

Real estate has unique tax rules since, like art, it has to be appraised. You can't definitively say what a building on East 57th Street in Manhattan is worth in the same way that you can quote the price of a share of IBM stock. The appraisal will determine the property's value and, thus, the taxes you owe on your ownership and transfer of the property.

The IRS tries to ensure these appraisals are independent. But you can only go so far. The Trumps, according to The Times account, got themselves an extraordinarily friendly appraiser.

Another tactic they relied on involves control of the partnerships through which real estate is often owned. When you determine the value of an interest in a partnership, the interest is worth less -- it's valued at a discount -- if it comes without control. The Trumps arranged ownership of their properties so that Fred got the discount. Because his interests in his properties were assigned a lower value, he paid less tax on it.

There are parts of this con job for which our president will never be called to account. No one will go to jail for the tax schemes.

There were reportedly other Trump tax reduction techniques. Fred Trump didn't just put his children on his payroll so he could claim his payments to them as business expenses. He also made his children the holders of his property mortgages, rather than working with conventional lenders. His mortgage payments on his buildings went to his kids.

In addition, instead of transferring property interests openly to his children, he transferred them to trusts that covertly benefited them. He extended loans, especially loans to Donald, that were never repaid. He sold property to Donald at a price that made the property a gift.

The other long con also masked Fred's help to his children. He was regularly spending large sums buying goods and services from contractors to maintain and improve his properties. So he set up a company, All County Building Supply & Maintenance, controlled by his children. Fred would pay All County instead of paying the contractors directly. But the All County's invoices to Fred were padded by 20 percent or more. The markups went to the Trump children.

There is no statute of limitations on the complicated con job that The New York Times laid out in its huge, document-laden investigation of Donald Trump's finances.

Trump and his father, real estate developer Fred Trump, used some accounting techniques that look a lot like civil tax fraud. If it is, that could lead to payments of up to 75 percent of the amount underpaid. Trump and his siblings could be forced to surrender, or "disgorge," many millions of dollars -- perhaps hundreds of millions -- in back taxes, fines and penalties to New York state alone.

The Times describes decades of what is politely called "creative accounting." Though the means were complicated, the purpose wasn't: Fred transferred $1 billion to his children, The Times estimates, and paid roughly 5 percent in estate taxes instead of the then-standard 55 percent.

How did they do this? First, the Trumps dramatically undervalued their property, which low-balled the amount of tax they had to pay. They also allegedly devised a whole other kind of fraud, according to The Times, padding virtually all maintenance invoices, so that Fred could list payments to his children as business expenses instead of taxable gifts.

These inflated bills also allowed the Trumps to increase the rents that they charged the low-income tenants in their government-subsidized housing developments. Tenants who could ill afford the rent hikes.

Just as serious -- if not qualifying as civil tax fraud -- is the fraud Donald Trump perpetrated on the American public. As a stripling golden-haired playboy, Trump presented his father's wealth as his own. He then used this claim to create an inflated impression of his own success and, ultimately, made it the basis of his presidential campaign.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it. Tax advisers routinely help clients toward this goal -- mainly in ways that are legal. They see to it that their clients make annual gifts to their children and grandchildren up to the amounts exempt from gift taxes. When the clients pass to their eternal reward, these amounts are then excluded when tallying estate taxes.

Something about having a large amount of money causes many wealthy people to decide the government shouldn't get any of it.

There are many other ways to avoid paying the government. Tax advisers, for example, see to it that clients, instead of making gifts to family members for tuition, pay the schools directly. The advisers make sure that clients make maximum use of their tax loss "carryforwards," so that the losses are spread over future years -- and offset any future gains.

And that's not counting the techniques that will put clients under the Internal Revenue Service microscope, like offshore investments and family limited partnerships. Advisers sometimes devise extremely sophisticated write-offs. Trump's sound relatively simple.

Real estate has unique tax rules since, like art, it has to be appraised. You can't definitively say what a building on East 57th Street in Manhattan is worth in the same way that you can quote the price of a share of IBM stock. The appraisal will determine the property's value and, thus, the taxes you owe on your ownership and transfer of the property.

The IRS tries to ensure these appraisals are independent. But you can only go so far. The Trumps, according to The Times account, got themselves an extraordinarily friendly appraiser.

Another tactic they relied on involves control of the partnerships through which real estate is often owned. When you determine the value of an interest in a partnership, the interest is worth less -- it's valued at a discount -- if it comes without control. The Trumps arranged ownership of their properties so that Fred got the discount. Because his interests in his properties were assigned a lower value, he paid less tax on it.

There are parts of this con job for which our president will never be called to account. No one will go to jail for the tax schemes.

There were reportedly other Trump tax reduction techniques. Fred Trump didn't just put his children on his payroll so he could claim his payments to them as business expenses. He also made his children the holders of his property mortgages, rather than working with conventional lenders. His mortgage payments on his buildings went to his kids.

In addition, instead of transferring property interests openly to his children, he transferred them to trusts that covertly benefited them. He extended loans, especially loans to Donald, that were never repaid. He sold property to Donald at a price that made the property a gift.

The other long con also masked Fred's help to his children. He was regularly spending large sums buying goods and services from contractors to maintain and improve his properties. So he set up a company, All County Building Supply & Maintenance, controlled by his children. Fred would pay All County instead of paying the contractors directly. But the All County's invoices to Fred were padded by 20 percent or more. The markups went to the Trump children.